Are you tired of imagining owning your own home? You’re not alone

With rising student debt, strict credit score demands, and the ever-rising cost of living, saving for a house seems unbeatable for many Canadians. But fear not! There’s hope in the financial confusion: down payment assistance programs.

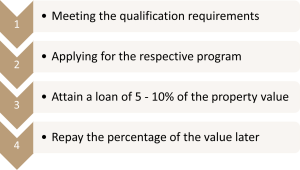

Lenders are working to help you save for a down payment. They operate on a shared equity model, meaning lenders share your property’s gains and losses. While there’s often a waiting list for these programs, successful applicants can secure 5-15% of the property value to put toward their down payment. The best part? You only need to pay back this percentage 20 years down the line or when you sell the property. If you’re ready to turn your homeownership dreams into reality, these programs might be the solution you’ve been searching for. Stick around to learn how you can benefit from these game-changing initiatives.Shared equity mortgageIn a shared equity mortgage, the homebuyer agrees to repay the amount the other party put in when selling the home. No interest is owed on this amount. Instead, the other party gets back their contribution for the down payment and a share of the sale proceeds. Their stake is in how much the home’s value increases or decreases. If the home’s value goes down, they might get back less than they put in.

Down Payment Assistance Programs and Uninsured Mortgages

In Canada, if you’re aiming for a mortgage with less than a 20% down payment, it must typically be insured. That’s a rule set by OSFI, the financial institution regulator. However, there’s good news: certain down payment assistance programs let you put down less than 20%. But here’s the critical question: will you still need mortgage default insurance?

In 2022, OSFI made it clear that federally regulated financial institutions can provide uninsured mortgages with shared equity under specific conditions:

- The mortgage holds the primary lien.

- The down payment assistance isn’t a loan.

You could put down as little as 5% and use a down payment assistance program to secure an uninsured mortgage if the equity provider boosts the total down payment to at least 20%. The strategy helps sidestep the expense of CMHC insurance and some CMHC mortgage restrictions.

Who is Eligible for Down Payment Assistance?

You must meet certain criteria to be eligible for down payment assistance programs. These programs specifically aim to help low to moderate-income families achieve homeownership. The qualifications are stringent, but you can navigate the process successfully with determination and the correct information.

Here are the requirements to qualify for these programs:

- Household Income: Your household income must fall within the low to moderate range, less than $100,000 annually.

- Purchase Price Limit: The house you intend to buy must be below a specified maximum price, typically less than $500,000.

- Mortgage Pre-Qualification: You must pre-qualify for a mortgage, demonstrating your ability to manage the financial responsibilities of homeownership.

- Residency Status: Assistance is only available to Canadian citizens and permanent residents.

- Primary Residence: The house you purchase must be your primary residence, not an investment property.

- First-Time Homebuyer Status: These programs are often reserved for first-time homebuyers, although there may be exceptions.

NOTE: The requirements can vary from one municipality to another as they tailor them to meet local needs. These programs undergo updates and changes regularly, so it’s wise to stay informed by checking the provided links for the latest information.

How to Get Down Payment Assistance in Canada

Federal Down payment Assistance Programs

Are you struggling with the down payment for your dream home? The First-Time Home Buyers Incentive (FTHBI) is here to help! You can borrow up to 10% of the total cost without adding to your monthly bills. It’s a shared equity loan, meaning you repay 10% of the property’s current value when you sell, not just what you borrowed.

Example: Buy a $400,000 house with a 10% FTHBI loan ($40,000). Sell for $500,000 later? You repay $50,000 (current value, not just borrowed amount).

To be eligible for the new FTHBI, you need to meet specific criteria:

- At least one owner must be a first-time homebuyer, meaning they haven’t owned a property or lived in one owned by their spouse in the last four years, unless due to a dissolved marriage.

- You must have a minimum down payment of 5%.

- Your combined household income must not exceed $120,000, including any income from co-signers or rental income.

- The amount of the mortgage must be at most $500,000.

- The mortgage-to-income ratio cannot surpass four times the household income, including any portion covered by the FTHBI.

Note: FTHBI helps you get in the door faster, but factor in the future repayment when deciding.

Ontario Down Payment Assistance Programs:

Kitchener (Region of Waterloo)

There’s never been a better moment to purchase a home in Kitchener. The municipality is financing 5% of the property value for first-time homebuyers. Homeowners who stay in their homes for over 20 years don’t need to repay the loan. But if you sell before 20 years, you must reimburse yourself for 5% of the house’s worth (same idea as FTHBI). You need to satisfy specific requirements, which you can see here. To be eligible, you should have resided in Waterloo for the last 12 months.

Barrie (Simcoe County)

If a qualified buyer meets the requirements, Simcoe County will lend up to 10% of the purchase price. Suppose applicants sell their property before 20 years. In that case, they will be required to repay the same proportion of the property value as in the case of Kitchener. Nevertheless, there is no obligation to repay the loan if the home has been used as the principal residence for over 20 years. Applicants require a family income of at least $75,100, and the house must not exceed $462,645. Further details on the program are available here.

Quebec Down Payment Assistance Programs

Montreal

Over 3,600 affordable condos have been created by Accès Condos across the city of Montreal. For an authorized development, buyers must pay a minimum of $1,000 in deposit and be given a 10% premium credit against their down payment.

Alberta Down Payment Assistance Programs

Calgary

Selected candidates under the Attainable Homes Program must only make a $2000 down payment on their homes. If the homeowner decides to sell, the program and the owner will divide the appreciation in value. Additionally, candidates have to pick from a pre-selected set of attributes. The homeowner must divide a smaller amount with the program the longer they reside there.

New Brunswick Down Payment Assistance Programs

A government-sponsored initiative called the Home Ownership Program offers first-time homeowners funding. As part of this project, a repayable loan of up to 40% of the purchase price of an existing home or $75,000 for new construction is given. Individuals with household earnings under $40,000 are eligible. It is not a shared equity mortgage. The interest rate is capped at the provincial borrowing rate, and the loan must be returned.

PEI Down Payment Assistance Programs

PEI’s Down Payment Assistance Program (DPAP) supports eligible residents with modest incomes in buying their first home. Through DPAP, you can receive a repayable loan of up to 5% of the property’s cost, with a maximum limit of $15,000, for either a new or existing home. This program is distinct from both shared equity mortgages and conventional mortgage loans. Your mortgage payments will directly reduce the principal amount. If, unfortunately, you default on payments, you’re responsible for repaying the outstanding balance along with accrued interest, calculated at 5% per year. Moreover, the home you’re purchasing must be, at most, a purchase price of $300,000.

Manitoba Down Payment Assistance Programs

The Rural Homeownership Program is open only to renters living in specific rural areas where Manitoba Housing has homes or those interested in buying vacant properties held by Manitoba Housing. Depending on whether you have children, your family income must be between $63,450 and $84,600 to qualify.

The program offers two types of loans:

- A 15% forgiving loan is granted after 15 years of continuous ownership and occupation.

- A 10% loan is forgiven proportionally over five years.

Exploring down payment assistance programs in Canada is crucial to avoid high mortgage costs. These programs offer valuable support, empowering potential homeowners to achieve their dreams without breaking the bank. By taking advantage of these initiatives, you can secure a brighter financial future and realize your goal of homeownership. Don’t miss out on the opportunity to access these resources and pave the way to affordable housing solutions. Take action today and unlock the path to owning your home confidently and quickly. Don’t wait any longer – take the first step towards securing your dream home by starting a conversation with your trusted financial advisor today!