The most useful real estate investing tips in Canada are usually the least flashy. Before you think about appreciation, you need to test affordability conservatively, confirm how a lender will treat rental income, understand the down payment and insurance rules for the property type, and make sure the property’s cash flow works in ordinary conditions.

Real estate investing often gets pitched as simple. Buy a property. Rent it out. Let the tenant cover the mortgage. Build wealth over time.

That version leaves out the hard part. In Canada, an investment property has to survive real underwriting rules, real carrying costs, real vacancies, and real market shifts. A deal that looks great in a quick video can fall apart once you add the mortgage stress test, property tax, insurance, repairs, condo fees, or stricter rental-income treatment.

This guide explains which real estate investing tips actually matter, how lenders look at rental properties, why cash flow matters more than hype, and what first-time investors should check before making an offer.

Want a quick reality check first? Run the deal using conservative rent, full monthly costs, and the lender’s actual rental-income method before you shop seriously.

Quick Start: Pick Your Path

- Buying your first investment property in Canada? Focus on down payment, stress-test affordability, and realistic cash flow.

- Looking at a condo rental? Focus on condo fees, resale risk, and your exit plan.

- Considering a duplex or triplex? Focus on rental-income treatment and maintenance risk.

- Planning to live in one unit and rent the rest? Focus on owner-occupied rules and how rent may be used in qualification.

- Counting on appreciation? Slow down and test whether the deal still works with flat prices and higher costs.

What Does Real Estate Investing Actually Mean in Canada?

Real estate investing means buying property mainly to earn rental income, build equity over time, capture appreciation, or some mix of all three. In Canada, that decision also changes the financing conversation because lenders, insurers, and regulators look closely at occupancy, down payment, rental income, and debt capacity.

An investment property is not just a property you like. It is a property whose financing, rent potential, expenses, and risk profile still make sense under lender rules.

For beginners, one rule matters more than almost anything else: if the deal only works when every assumption goes right, it is probably not a safe first investment.

Key takeaway: Real estate investing in Canada is a financing and cash-flow exercise before it becomes a wealth-building story.

Why Should Investors Watch Financing Rules So Closely?

Mortgage rules can change what looks affordable on paper. Down payment requirements, mortgage-insurance eligibility, and the stress test can all reduce borrowing power or change which properties are realistic.

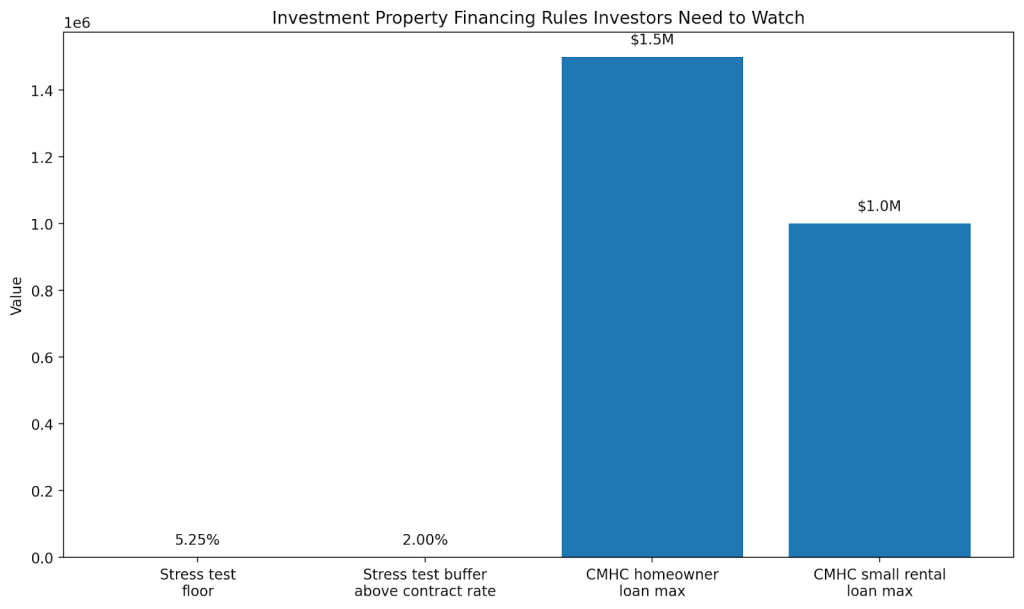

FCAC says federally regulated lenders generally qualify borrowers at the higher of 5.25% or the contract rate plus 2%. That means your real borrowing capacity may be lower than a basic mortgage payment estimate suggests.

CMHC’s consumer guidance says the maximum purchase price or lending value must be below $1.5 million for homeowner loans and $1 million for small rental loans if you want CMHC-insured mortgage financing. CMHC also says minimum down payments can start at 5% for qualifying homeowner purchases, while small rental financing has its own rules and may require more equity depending on the setup.

That is one of the most important real estate investing tips Canadian buyers miss: the property type, unit count, and occupancy plan can all change the financing path.

Here is what can shift the math quickly:

- Whether the property is owner-occupied or non-owner-occupied

- Whether mortgage insurance is available for that deal structure

- The number of units

- The lender’s stress-test calculation

- How the lender treats projected rent

Decision checkpoint: Before you fall in love with a deal, ask your broker which financing path applies to that exact property, not just to “investment properties” in general.

How Is Rental Income Treated for Mortgage Qualification?

Rental income can help with qualification, but lenders and insurers do not always count all of it the same way. The actual treatment depends on whether the property is owner-occupied or non-owner-occupied, whether the loan is insured, and which lender is reviewing the file.

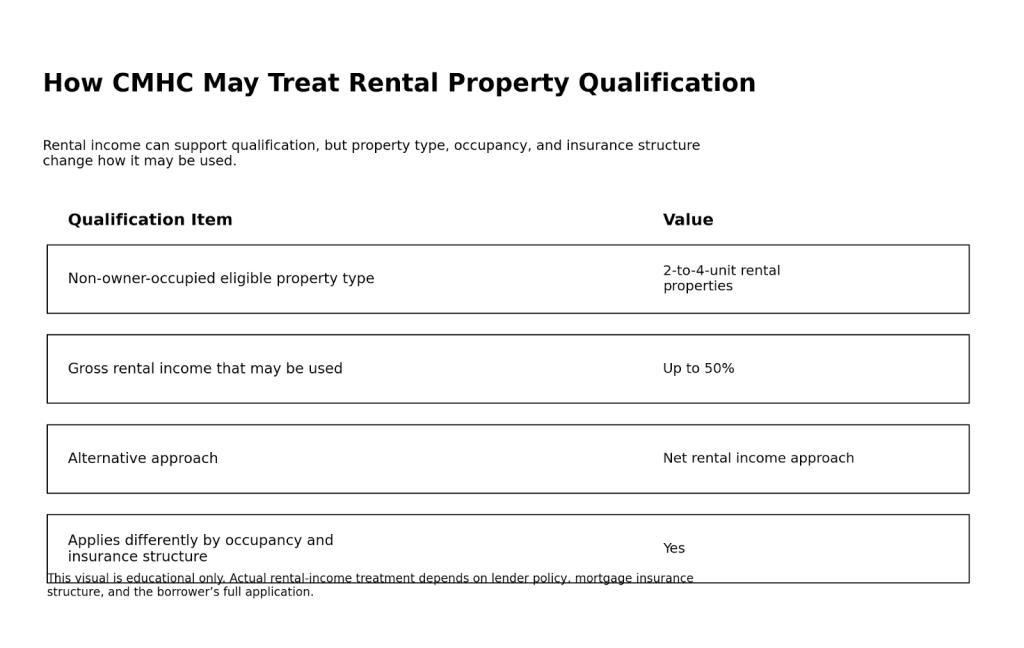

CMHC says it offers different approaches to rental income for qualification purposes depending on the situation. For example:

- For some owner-occupied 2-unit insured setups, CMHC allows up to 100% of gross rental income

- For some owner-occupied 3- to 4-unit insured setups, it may allow either up to 50% of gross rental income or a net rental income approach

- For non-owner-occupied 2- to 4-unit small rental loans, CMHC says borrowers may use up to 50% of gross rental income or a net rental income approach

OSFI also clarified in November 2025 that its rental-income communication was about mortgage classification and capital treatment for financial institutions, not a change to borrower qualification rules under Guideline B-20. In plain English, rental income can still be used, but you should not assume every lender will use it the same way.

That is why one of the most practical real estate investing tips is also one of the simplest: ask early how much of the property’s projected rent will actually count for qualification with your chosen lender.

Key takeaway: Expected rent is not the same as usable qualifying income.

Why Does Cash Flow Matter More Than Appreciation Hype?

Cash flow is the property’s ability to carry its own costs through rent and reserves. Appreciation is uncertain. A property with weak cash flow can become stressful very quickly if rents disappoint, rates stay elevated, or repairs arrive earlier than expected.

The Bank of Canada has found that mortgage stress tests improve borrower resilience to financial shocks. That matters for investors because leveraged buyers are more exposed when payments, vacancies, or carrying costs move in the wrong direction.

The Bank of Canada’s 2025 Financial Stability Report also says there are still pockets of financial stress in the economy, even though overall resilience has improved in some areas. And in February 2026, the Bank of Canada noted that Toronto condos are no longer providing substantial returns for short-term investors the way they once did, partly because population growth has eased and interest rates have risen.

For an investor, the practical lesson is clear. A deal should still make sense if:

- Rent grows slowly

- A vacancy happens

- Repairs come sooner than planned

- Refinancing is less attractive than hoped

- Resale takes longer than expected

Decision checkpoint: If the property only works when appreciation saves the deal, the risk may be higher than it first appears.

What Should You Watch in Condos, Duplexes, and Small Rentals?

Each property type carries a different risk mix.

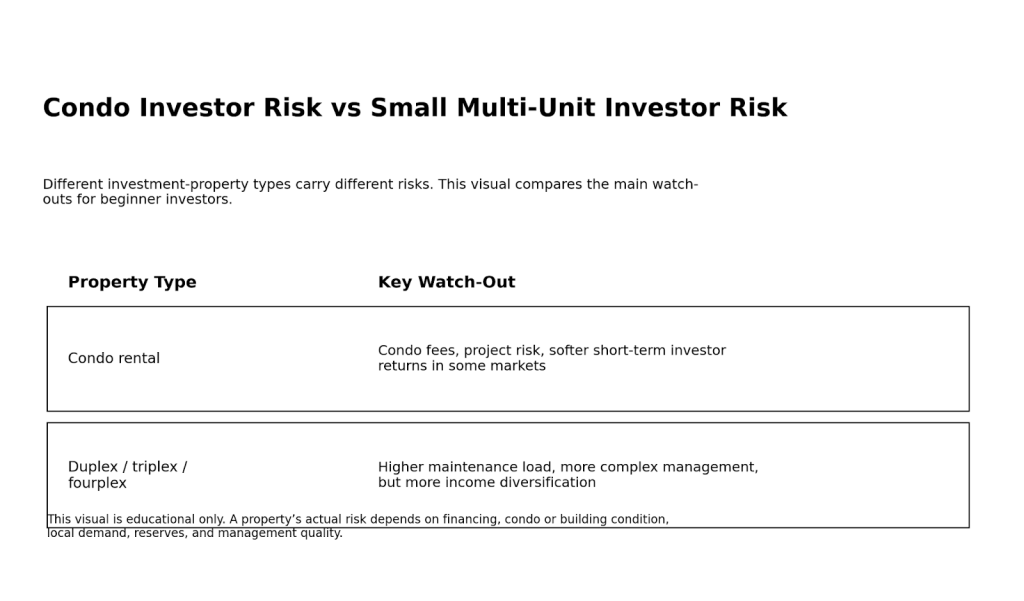

A condo can feel beginner-friendly because the entry price may be lower and some exterior maintenance is handled by the condo corporation. But that simplicity comes with trade-offs. Condo fees can compress cash flow, project-level issues can affect resale and financing, and certain markets can become more volatile for investors.

A duplex, triplex, or fourplex may offer better income diversification because one vacancy does not reduce income to zero. But it can also bring more direct maintenance responsibility, more moving parts in underwriting, and higher day-to-day management demands.

| Feature | Condo Rental | Duplex / Triplex / Fourplex |

| Entry complexity | Often simpler at first glance | Usually more complex |

| Income diversification | One tenant | Multiple rent streams |

| Fee exposure | Condo fees may reduce cash flow | No condo fees, but more direct maintenance responsibility |

| Market risk | More exposed to condo resale and project conditions | More exposed to property management and repair execution |

| Best for | Investor prioritizing simplicity and lower operational load | Investor prioritizing income spread and rental flexibility |

In Ontario especially, condo investors should pay attention to fees, reserve pressure, and resale conditions. The Bank of Canada’s 2026 Toronto condo analysis is a reminder that short-term investor returns can weaken when demographics, rates, and supply change.

Key takeaway: “Easy to buy” is not the same as “safe to hold.”

A Practical Roadmap Before Buying an Investment Property in Canada

The safest way to start is to underwrite the deal before you fall in love with the property.

Use this sequence:

- Get pre-qualified or pre-approved and ask how investment-property rules differ from an owner-occupied purchase

- Confirm down payment and insurance rules for the exact property type and occupancy plan

- Ask how rental income will be counted by the lender you are actually using

- Build a full monthly cost estimate including mortgage payment, taxes, insurance, utilities you cover, condo fees if applicable, repairs, and vacancy allowance

- Review the local market, not just national headlines

- Decide your exit strategy before you buy: hold, refinance later, or sell if conditions change

- Keep reserves so one vacancy or repair does not force a panic sale

Why Professional Help Matters

A simple investment calculator cannot tell you how a lender will treat rent, whether a property still works after the stress test, or whether a condo’s cash flow is too thin for your risk tolerance.

That is where tailored mortgage guidance helps. A mortgage professional can help you:

- Compare owner-occupied and non-owner-occupied financing paths

- Test the deal using the lender’s actual rental-income method

- Pressure-test debt ratios under the stress test

- Spot when a property’s cash flow is too dependent on ideal conditions

At Pegasus, the goal is not to sell a story. It is to help you judge whether the property is realistic under current mortgage rules.

Example Scenario

A first-time investor was deciding between a Toronto condo and a small duplex. The condo looked easier to enter, but once condo fees, softer resale conditions, and thinner monthly margins were included, the numbers became less forgiving. The duplex involved more management, but the second unit created a more diversified income stream and a more durable cash-flow picture.

Common Mistakes First-Time Investors Make

Most beginner errors come from underestimating carrying costs and overestimating certainty.

Common mistakes include:

- Assuming the property will qualify based on full market rent

- Forgetting the stress test

- Buying for appreciation only

- Ignoring condo project and resale risk

- Underestimating down payment requirements

- Running with no reserve fund

- Using national averages as if they were local facts

Key takeaway: The downside usually shows up in the details investors rush past.

FAQ

Is buying an investment property in Canada harder than buying a primary home?

Often, yes. Investment-property financing can involve different equity expectations, different insurance rules, and stricter treatment of rental income.

Do all lenders count rental income the same way?

No. Rental income treatment varies by lender, property type, occupancy plan, and whether the loan is insured.

Is a condo a good first investment property in Canada?

Sometimes, but not automatically. A condo may be easier to enter, yet it can come with condo fees, project-level risk, and softer short-term investor economics in some markets.

What is the safest real estate investing tip for beginners?

Buy a property that still works under conservative assumptions. That means realistic rent, realistic costs, a reserve fund, and an affordability check that includes the stress test.

Can I buy a rental property with mortgage insurance in Canada?

Sometimes, yes. CMHC offers insurance solutions for certain homeowner and small rental loans, including eligible non-owner-occupied 2- to 4-unit properties.

Should I focus on appreciation or cash flow?

For beginners, cash-flow discipline is usually safer than relying on appreciation. Monthly carrying costs are real. Price growth is not guaranteed.

What is one question every first-time investor should ask a mortgage broker?

Ask: How will this lender treat the property’s rental income in my qualification? That answer can materially change what you can buy and whether the deal is workable.

Final Thoughts

The best real estate investing tips are usually the least dramatic. Check the financing rules. Check the rental-income math. Check the reserve plan. Check whether the deal still works when conditions are ordinary, not perfect.

For Ontario and Canada-wide buyers, that matters even more in 2026. Investor activity, condo conditions, and mortgage affordability are all more nuanced than a simple “buy and wait” story suggests. A careful investor underwrites the downside before betting on the upside.

- Check the financing path

- Check the rental-income treatment

- Check the full monthly carrying cost

- Check your reserve cushion

- Check whether the exit plan still makes sense if the market softens

If you want help checking whether an investment property is realistic under current mortgage rules, speak with a Pegasus mortgage professional before you make an offer.

Sources & References

- Financial Consumer Agency of Canada, Preparing to get a mortgage

https://www.canada.ca/en/financial-consumer-agency/services/mortgages/preparing-mortgage.html - Office of the Superintendent of Financial Institutions, Clarifying OSFI’s guidance on rental income and mortgage classification

https://www.osfi-bsif.gc.ca/en/risks/real-estate-secured-lending/clarifying-osfis-guidance-rental-income-mortgage-classification - CMHC, Rental Income

https://www.cmhc-schl.gc.ca/professionals/project-funding-and-mortgage-financing/mortgage-loan-insurance/mortgage-loan-insurance-homeownership-programs/rental-income - CMHC, Income Property

https://www.cmhc-schl.gc.ca/professionals/project-funding-and-mortgage-financing/mortgage-loan-insurance/mortgage-loan-insurance-homeownership-programs/income-property - CMHC, General requirements to qualify for homeowner mortgage loan insurance

https://www.cmhc-schl.gc.ca/consumers/home-buying/mortgage-loan-insurance-for-consumers/what-are-the-general-requirements-to-qualify-for-homeowner-mortgage-loan-insurance - Bank of Canada, Financial Stability Report 2025

https://www.bankofcanada.ca/2025/05/financial-stability-report-2025/ - Bank of Canada, Mortgage stress tests and household financial resilience

https://www.bankofcanada.ca/2024/11/staff-analytical-note-2024-25/ - Bank of Canada, What’s behind the slowdown in Toronto’s condo market

https://www.bankofcanada.ca/2026/02/sparks-at-bank-article-2026-2/ - Bank of Canada, Housing demand in Canada: A novel approach to categorizing homebuyers

https://www.bankofcanada.ca/2022/01/staff-analytical-note-2022-1/ - Bank of Canada, Real estate market definitions, graphs and data

https://www.bankofcanada.ca/rates/indicators/capacity-and-inflation-pressures/real-estate-market-definitions/