A lot of Canadians searching for GST HST Credit are really trying to answer a different question: Can I save tax when I buy a home? That confusion makes sense. The regular GST/HST credit is a quarterly benefit for eligible people and families with low or modest incomes. It is real, but it is not the same thing as the rebate tied to buying a newly built or substantially renovated home.

In 2026, that distinction matters even more. The CRA is now accepting applications for the new first-time home buyers’ GST/HST rebate, which can refund up to the full federal GST, or the federal part of the HST, on qualifying new homes valued up to $1 million, with a phase-out on homes between $1 million and $1.5 million.

This guide explains what the GST HST Credit is, how it differs from the new homebuyer rebate, how much a first-time buyer may save, and what Ontario buyers should understand before building those savings into a purchase budget.

Need the fastest answer? If you are buying a resale home, the new first-time home buyers’ GST/HST rebate usually does not apply. If you are buying a new or substantially renovated home, it might.

Quick Start: Pick Your Path

- Buying a resale home? The new federal first-time home buyers’ rebate usually does not apply.

- Buying a newly built home from a builder? Focus on the new federal rebate, the existing new housing rebate, and any provincial rebate rules.

- Building your own home? You may still qualify, but the forms and timing are different.

- Buying in Ontario? Pay close attention to the difference between Ontario’s existing rebate and newer proposed full provincial HST relief.

- Not sure whether you are truly a first-time buyer? Check the current year plus previous four calendar years rule before relying on any estimate.

What Changed for Buyers in 2026?

The biggest update is that the CRA is now accepting applications for the new first-time home buyers’ GST/HST rebate.

This federal rebate can remove up to 100% of the federal GST, or the federal part of the HST, on qualifying new homes valued up to $1 million. It then phases down on homes between $1 million and $1.5 million. At or above $1.5 million, there is no rebate under this specific federal first-time buyer program.

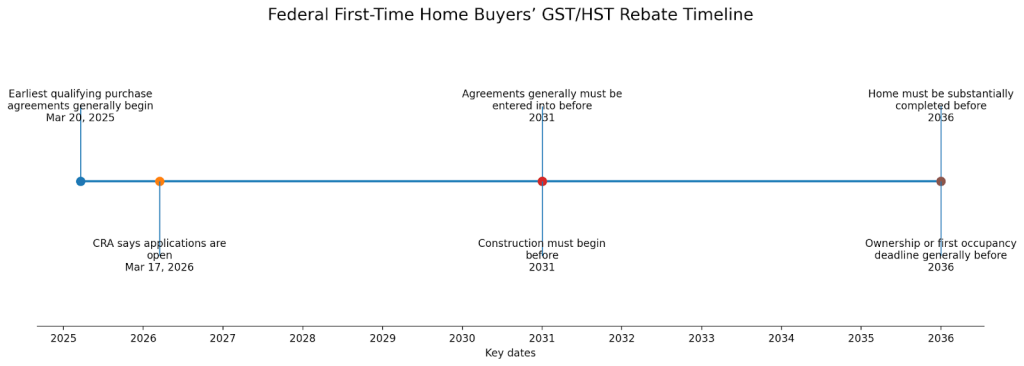

The federal government says the rebate generally applies to agreements of purchase and sale entered into on or after March 20, 2025, and before 2031, with construction beginning before 2031 and substantial completion before 2036.

The CRA also says applications are now open, although it is still updating systems for some earlier agreements signed between March 20, 2025 and May 26, 2025.

Key takeaway: For many first-time buyers in 2026, the biggest tax savings are coming from the new first-time home buyers’ GST/HST rebate, not the regular GST/HST credit.

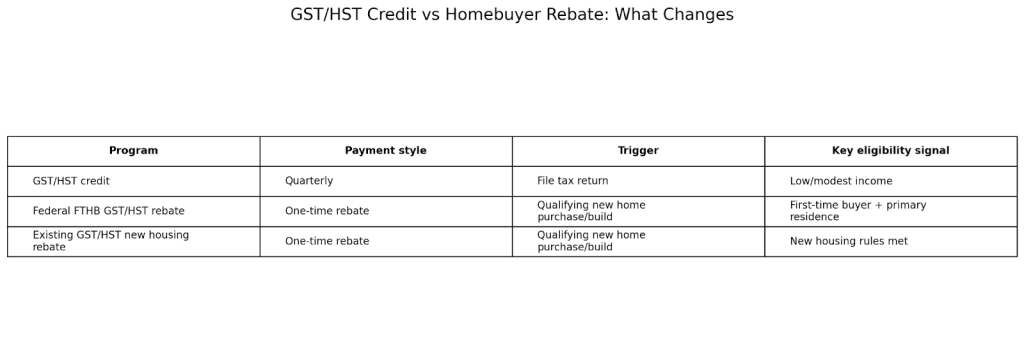

What Is the GST/HST Credit, and Why Is It Different?

The regular GST HST Credit is a tax-free quarterly payment for eligible individuals and families with low or modest incomes. It is not a home-purchase rebate.

The CRA automatically considers you for the GST/HST credit when you file your tax return. For 2026, the CRA lists the payment dates as:

- January 5

- April 2

- July 3

- October 5

The new first-time home buyers’ GST/HST rebate is different. It is tied to buying, building, or substantially renovating a qualifying first home. It is based on the property and transaction, not mainly on your annual income.

That is the distinction many buyers miss.

- GST/HST credit: recurring quarterly benefit for eligible households

- First-time home buyers’ GST/HST rebate: transaction-based refund tied to a qualifying new home

Key takeaway: The GST/HST credit helps with cost of living. The first-time home buyers’ GST/HST rebate helps with the tax cost of a qualifying new home purchase.

Who May Qualify for the New Federal Rebate?

To qualify, a buyer generally must:

- Be at least 18 years old

- Be a Canadian citizen or permanent resident

- Meet the first-time home buyer test

- Buy or build a newly built or substantially renovated home

- Intend to use the home as their primary place of residence

The first-time buyer test is stricter than many people expect.

The CRA says you generally must not have lived in a home that you or your spouse or common-law partner owned, in Canada or outside Canada, as your primary residence during:

- The calendar year you take ownership, and

- The previous four calendar years

The CRA also says neither you nor your spouse or common-law partner can have already received this specific first-time home buyers’ GST/HST rebate.

The home must usually be:

- Newly built or substantially renovated

- Intended as your primary place of residence

- The first home occupied after construction or substantial renovation is completed, depending on the situation

The CRA’s substantial-renovation rule is also important. In general, 90% or more of the interior must be removed or replaced. A cosmetic update does not count.

Key takeaway: This rebate is for a true first-time buyer buying or building a qualifying new or substantially renovated home for real owner-occupancy.

How Much Could You Save?

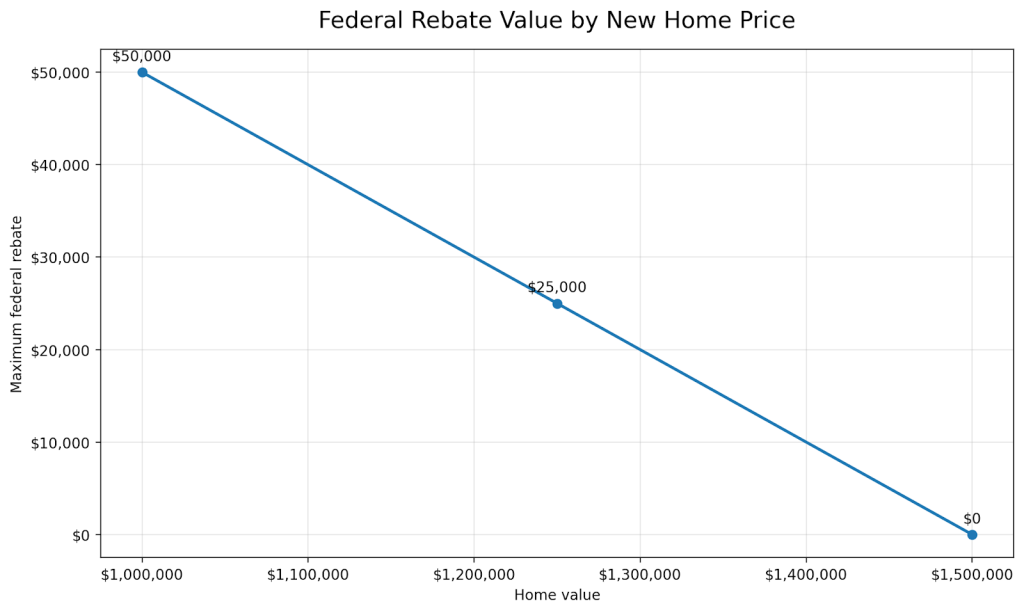

The maximum federal first-time home buyers’ GST/HST rebate is up to $50,000.

Here is the practical framework:

- Home value up to $1 million: up to the full federal GST or federal part of HST may be refunded

- Home value between $1 million and $1.5 million: rebate phases down

- Home value at or above $1.5 million: no rebate under this program

The CRA gives a helpful example: a qualifying buyer purchasing a new home for $1.25 million is at the midpoint of the phase-out band, so they may receive 50% of the maximum rebate, or $25,000, if all conditions are met.

Decision checkpoint: If you are shopping close to the $1 million or $1.5 million thresholds, a small price difference can materially change the federal rebate result.

How Does This Compare With Existing Rebates in Ontario?

Ontario buyers need to separate three different ideas:

- The regular GST/HST credit

- The new federal first-time home buyers’ GST/HST rebate

- Ontario’s existing new housing rebate, plus any newer provincial proposal

Here is the simple comparison:

| Feature | GST/HST credit | Federal first-time home buyers’ GST/HST rebate | Existing GST/HST new housing rebate | Ontario proposed new full HST relief |

| Main purpose | Quarterly cost-of-living benefit | Reduce federal GST on qualifying first homes | Refund some GST/HST on qualifying new homes | Proposed extra provincial HST relief for first-time buyers |

| Who it helps | Low- and modest-income individuals and families | Eligible first-time buyers of qualifying new homes | Eligible buyers or owner-builders of qualifying new homes | First-time buyers of qualifying new homes in Ontario |

| Based on income? | Yes | Not mainly | Not mainly | Not mainly |

| Applies to resale homes? | Not tied to home type | Generally no | Generally no | Proposed for qualifying new homes |

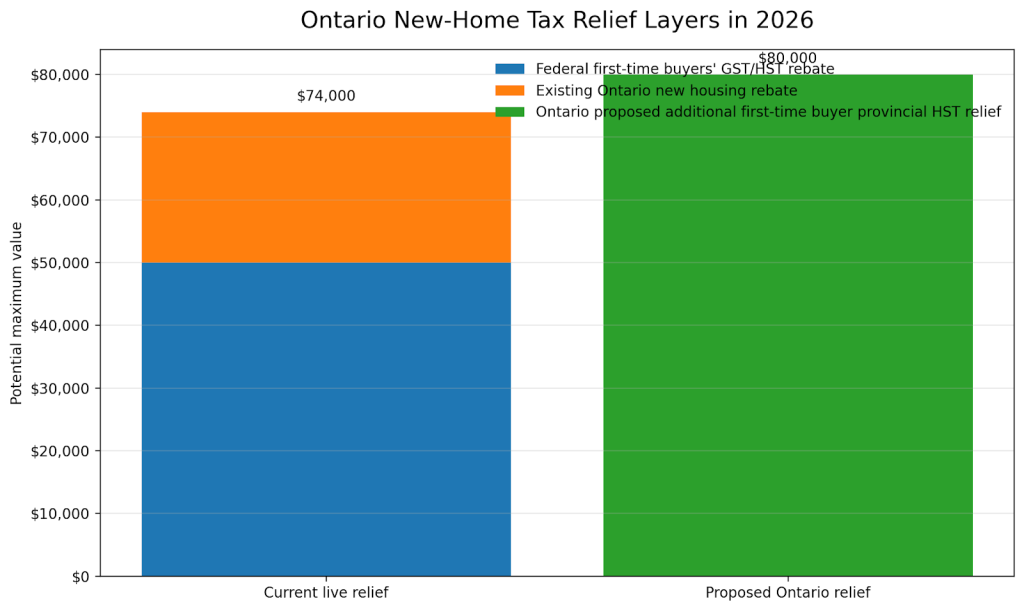

| Key current max | Varies by income and family size | Up to $50,000 | Federal and possible provincial components may apply | Province has described up to $80,000 in combined provincial relief for qualifying buyers |

| Current official status | Live | Live | Live | Still described by Ontario as proposed |

For Ontario specifically, CRA says the existing Ontario new housing rebate may be available for some of the provincial part of the HST, and CRA’s Ontario rebate schedule reflects a maximum of up to $24,000 in relief under the existing provincial rebate structure.

Ontario’s newer broader relief for first-time buyers is different. Ontario announced in October 2025 that it was proposing to rebate the full 8% provincial portion of the HST for first-time buyers on qualifying new homes valued up to $1 million, but official Ontario sources still describe that measure as a proposal tied to the 2025 Fall Economic Statement.

Key takeaway: Ontario buyers should not treat the newer full provincial HST relief as a confirmed live program unless official implementation details say it is in force.

What Does “Primary Place of Residence” Mean?

For rebate purposes, the CRA generally treats a primary place of residence as the home you live in on a permanent basis. You can own or use more than one residence, but you are considered to have only one primary place of residence.

This matters because these rebate programs are meant for owner-occupants, not pure investors.

If you plan to:

- Flip the home quickly

- Rent it out immediately

- Leave occupancy unclear

then your rebate position may become weaker.

Buyers should make sure the purchase contract, mortgage file, builder paperwork, and actual move-in facts all tell the same story.

Key takeaway: The rebate is meant for a home you genuinely intend to live in as your main home.

How to Claim the Rebate

The process depends on whether you bought from a builder or built the home yourself.

In some builder deals, the builder may credit the rebate at closing. If not, you may need to apply directly to the CRA.

Step-by-step roadmap

- Confirm the home type. Check whether the property is newly built, substantially renovated, owner-built, or resale.

- Check first-time buyer status early. Review the current calendar year plus the prior four calendar years for you and your spouse or common-law partner.

- Review the purchase price band. Below $1 million, between $1 million and $1.5 million, or at or above $1.5 million changes the federal result.

- Ask the builder whether the rebate will be credited at closing. The CRA says builders may credit the federal rebate in the same manner as the existing new housing rebate.

- If not credited, apply directly. The CRA says buyers may apply through their CRA account or by mailing the correct form.

- Use the right form. Homes purchased from a builder generally use Form GST190. Owner-built homes generally use Form GST191.

- Watch the deadline. The CRA says there is usually a two-year time limit to apply after taking ownership or after substantial completion, depending on the situation.

- Keep your proof. Save the agreement of purchase and sale, occupancy records, invoices, and builder statements.

Decision checkpoint: Ask about the rebate before closing, not after. In some transactions, that changes whether the builder credits it up front or you wait to recover it later.

Common Mistakes Buyers Make

Most problems come from mixing programs together or assuming a proposal is already live.

Common mistakes include:

- Confusing the GST/HST credit with the homebuyer rebate

- Assuming resale homes qualify

- Ignoring the spouse or common-law partner ownership rule

- Missing the four prior calendar years test

- Treating Ontario’s newer full HST relief as already in force

- Forgetting the primary-residence requirement

- Failing to ask whether the builder will credit the rebate at closing

Key takeaway: The biggest rebate mistakes usually happen before the purchase closes, not after.

FAQ

Does the GST/HST credit help me buy a house?

Not directly. The GST HST Credit is a quarterly tax-free benefit for eligible low- and modest-income households. It is different from the new homebuyer rebate tied to qualifying new home purchases.

Can I get the federal rebate on a resale home?

Usually not. The first-time home buyers’ GST/HST rebate is generally for newly built or substantially renovated homes, certain co-op units, and some owner-built situations.

How much is the maximum federal savings?

The maximum federal first-time buyer rebate is up to $50,000 on a qualifying new home valued at or below $1 million.

What happens if the home costs more than $1.5 million?

There is no federal first-time home buyers’ GST/HST rebate at or above $1.5 million.

Can Ontario buyers still get provincial relief?

Yes. Ontario buyers may still qualify for the existing Ontario new housing rebate. But the newer broader Ontario first-time buyer HST relief is still officially described by Ontario as a proposal.

Who counts as a first-time home buyer?

Generally, you must not have lived in a home that you or your spouse or common-law partner owned as your primary residence during the year you take ownership and the previous four calendar years.

How do I claim the rebate if the builder does not credit it at closing?

The CRA says you may apply directly through your CRA account or by mailing the correct rebate form. Homes purchased from a builder generally use Form GST190, while owner-built homes generally use Form GST191.

Is there a deadline to apply?

Usually yes. The CRA says there is generally a two-year limit from taking ownership or finishing construction, depending on the situation.

Final Thoughts

The big takeaway is simple: when buyers search GST HST Credit in 2026, many are really asking about new-home tax rebates.

For first-time buyers purchasing a qualifying new or substantially renovated home, the new federal rebate may be worth real money. For Ontario buyers, there may also be provincial relief, but you need to separate current live rebates from newer proposals before you build those savings into your budget.

- Confirm whether the home is new or substantially renovated

- Check the first-time buyer test early

- Watch the $1 million and $1.5 million thresholds

- Ask whether the builder credits the rebate at closing

- Treat Ontario’s newer full HST relief as proposed unless official sources say it is in force

If you are budgeting for a newly built home, speak with a mortgage professional early so you can understand how any rebate may affect your down payment strategy, cash needed at closing, and overall affordability.

Sources & References

- https://www.canada.ca/en/revenue-agency/services/child-family-benefits/gst-hst-credit.html

- https://www.canada.ca/en/revenue-agency/services/child-family-benefits/gst-hst-credit/payment-dates.html

- https://www.canada.ca/en/revenue-agency/services/child-family-benefits/gst-hst-credit/who-eligible.html

- https://www.canada.ca/en/revenue-agency/services/child-family-benefits/gst-hst-credit/get-credit.html

- https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses/gst-hst-rebates/first-time-home-buyers-gst-hst-rebate.html

- https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses/gst-hst-rebates/first-time-home-buyers-gst-hst-rebate/what-rebate.html

- https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses/gst-hst-rebates/first-time-home-buyers-gst-hst-rebate/who-can-apply.html

- https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses/gst-hst-rebates/first-time-home-buyers-gst-hst-rebate/how-apply.html

- https://www.canada.ca/en/revenue-agency/news/newsroom/tax-tips/tax-tips-2026/first-time-buyers-can-save-more-on-new-homes-the-first-time-home-buyers-gst-hst-rebate-is-available-now.html

- https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/gst-hst-businesses/gst-hst-rebates/new-housing-rebate.html

- https://www.canada.ca/en/department-finance/news/2026/03/legislation-to-make-life-more-affordable-receives-royal-assent.html

- https://news.ontario.ca/en/release/1006665/ontario-lowering-costs-for-first-time-home-buyers

- https://budget.ontario.ca/2025/fallstatement/chapter-1b-costs.html

- https://www.ontario.ca/document/land-transfer-tax