Many Canadian buyers can afford a monthly payment but still struggle to qualify for a mortgage on paper. The issue may be income, debt ratios, credit history, or the size of the loan needed in today’s market.

That is when families often ask the same question: should we use a guarantor or a co-signer?

The two terms are often used loosely in conversation, but they are not always the same in mortgage underwriting or legal documents. One option usually gives the lender a joint borrower. The other may create a separate guarantee obligation. Either way, the person helping is taking on real financial risk.

This guide explains the difference in plain English, how lenders and mortgage insurers usually view each structure, what 2026 mortgage rules still apply, and what both the buyer and the helper should understand before signing anything.

Want a fast first filter? Start by asking the lender one direct question: are you proposing a joint-borrower structure or a guarantee structure?

Quick Start: Pick Your Path

- First-time buyer with limited income: Read the sections on approval and stress testing.

- Parent or relative helping with a mortgage: Read the risk and responsibility sections carefully.

- Buyer using less than 20% down: Focus on insured-mortgage rules and eligibility.

- Buyer with 20% or more down: Focus on lender underwriting and the stress test.

- Anyone unsure who should go on title: Read the comparison table first.

What Is a Guarantor, and What Is a Co-Signer?

A co-signer is usually a joint borrower who signs the mortgage and becomes equally responsible for the debt. A guarantor also supports the loan, but usually does so by promising to cover the debt if the borrower defaults, without always being treated the same way as a joint borrower.

FCAC gives the clearest consumer-facing definition of co-signing. It says a joint borrower is someone who signs a mortgage, loan, credit card, or line of credit agreement with another person, and that this is also referred to as co-signing. FCAC also says the joint borrower becomes equally responsible for repaying the unpaid balance.

FCAC separately explains that co-borrowers have access to the account and are equally responsible for the balance, while guarantors are responsible for the balance without having account access. That guidance is not mortgage-specific, but it captures the core difference consumers need to understand.

At the insurer level, Sagen also treats guarantees and non-residing co-borrowers as different concepts in its underwriting materials. That supports the practical point that lenders and insurers may not use the two labels interchangeably.

Key takeaway: A co-signer is typically a joint borrower. A guarantor backs the debt, but is usually documented differently and may not have the same account access or ownership role.

How Do Lenders Usually Treat a Guarantor and a Co-Signer?

In practice, lenders usually treat a co-signer as part of the main borrowing group, while a guarantor is an added layer of support for the lender.

A co-signer is generally easier to explain in underwriting because that person is fully on the debt. A guarantor arrangement can still help, but it usually has to be enforceable and documented properly under provincial law.

Sagen says guarantees must be valid and fully enforceable in the event of default and must survive amendments or renewal of the mortgage. It also says lenders should consider provincial or territorial law and give guarantors the opportunity to receive independent legal advice.

That matters because family help is still legal exposure. Even when a parent or relative is only “helping out,” the guarantee is not symbolic.

Decision checkpoint: Never assume the lender means the same thing you mean when they say “guarantor” or “co-signer.” Ask how the file is actually being structured.

Does a Guarantor or Co-Signer Help Mortgage Approval in Canada?

Yes, a guarantor or co-signer may help a buyer qualify if the added support improves the application’s credit strength, income profile, or overall lender comfort. But help is not automatic.

Approval still depends on lender policy, debt ratios, credit, down payment, and whether the mortgage is insured or uninsured.

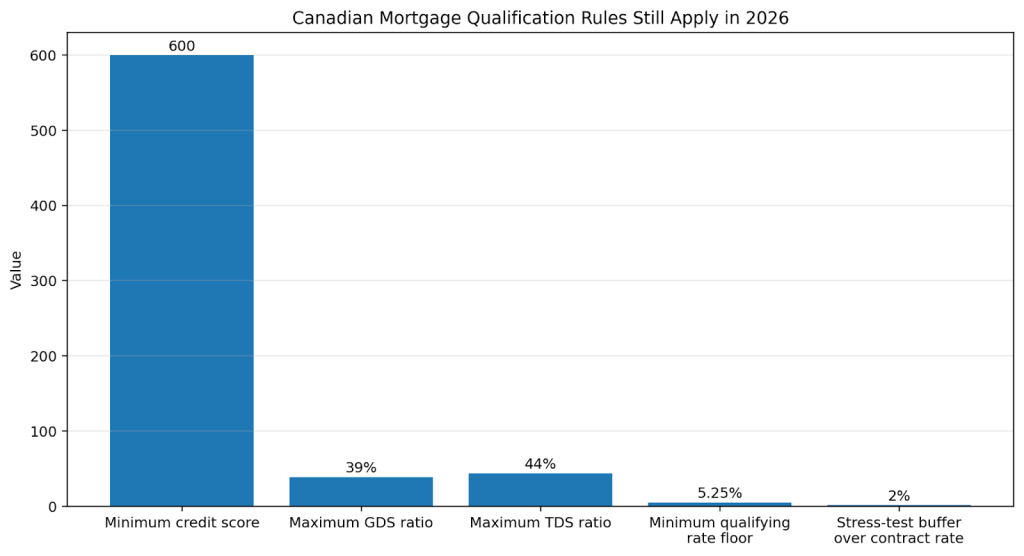

CMHC’s purchase criteria say at least one borrower or guarantor must have a minimum credit score of 600. CMHC also says insured purchase files must still satisfy debt-service limits and the qualifying rate.

That means the added person can strengthen the file, but cannot erase the core math of affordability.

Key takeaway: A guarantor may improve the strength of the file, but does not cancel the stress test, debt-ratio limits, or mortgage-insurance rules.

What 2026 Mortgage Rules Still Apply Even If Someone Helps You?

The big 2026 rules still apply whether you use a guarantor or a co-signer.

For uninsured mortgages, OSFI says the current minimum qualifying rate is the greater of the contract rate plus 2% or 5.25%. CMHC uses the same basic minimum qualifying-rate approach for insured purchase files.

CMHC also says insured purchase underwriting uses maximum debt-service thresholds of:

- 39% GDS

- 44% TDS

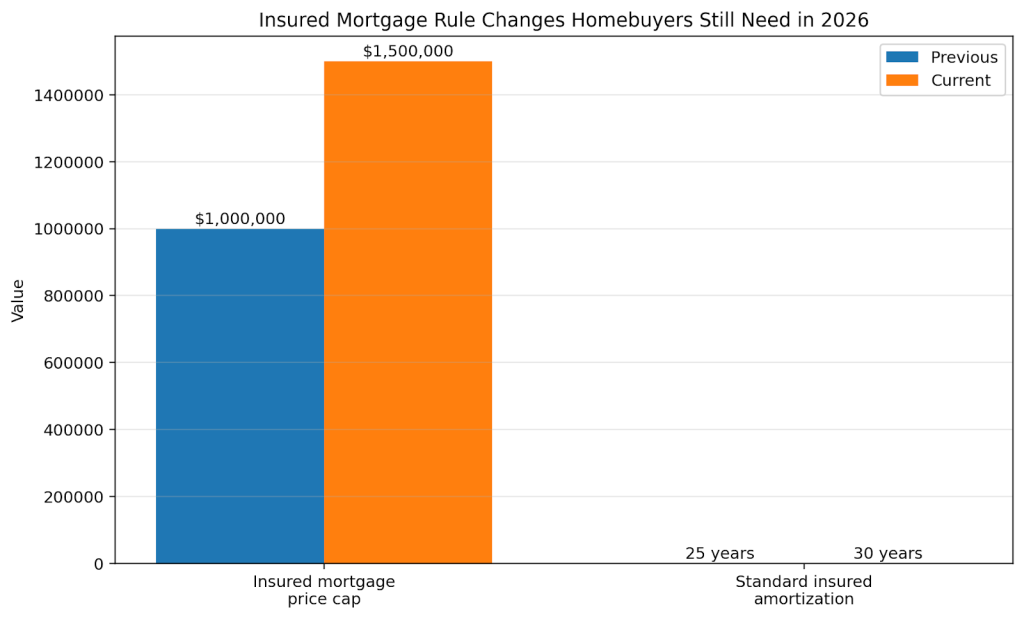

Recent federal reforms are still part of the 2026 environment. The Department of Finance says the insured-mortgage cap increased from $1 million to $1.5 million effective December 15, 2024. It also says 30-year insured amortizations are available to all first-time homebuyers and all buyers of new builds.

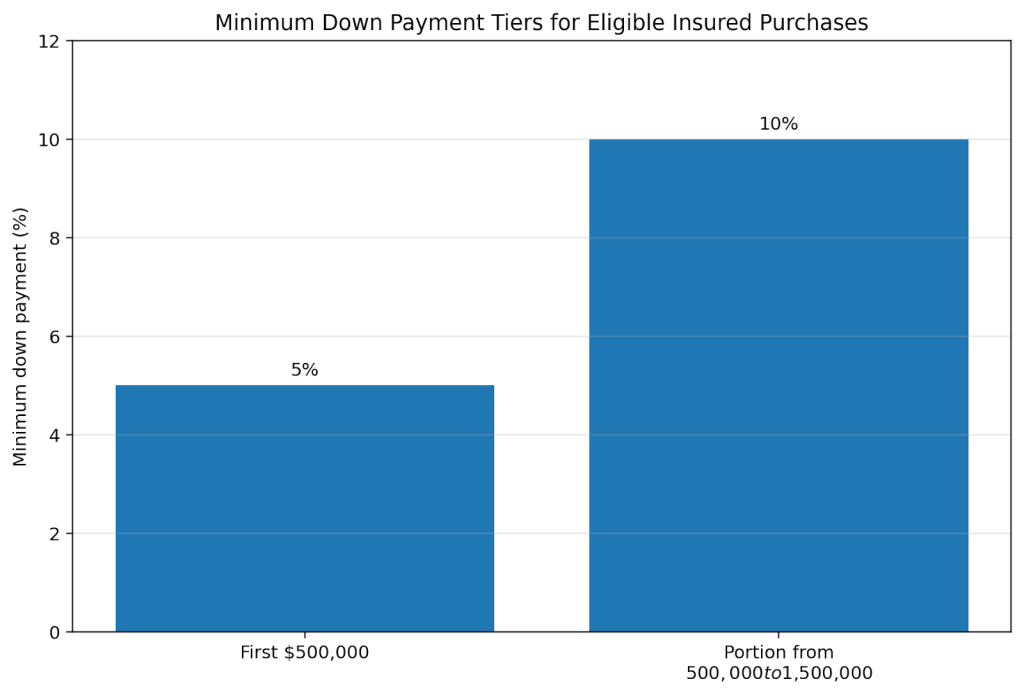

FCAC’s down-payment guidance reflects the current insured framework:

- 5% on the first $500,000 of the purchase price

- 10% on the portion between $500,000 and $1.5 million

These reforms may help some buyers, but they do not remove the need to qualify.

Key takeaway: Extra support can strengthen an application, but it does not create an exception to stress testing or insured-mortgage rules.

Which Option Is Usually Better: Guarantor or Co-Signer?

There is no universal winner.

A co-signer may be simpler when the lender wants a full joint borrower. A guarantor may work when the lender accepts a guarantee structure and the support person does not need the same borrower role.

The better choice is the one your lender and lawyer can document clearly and safely.

| Feature | Guarantor | Co-signer / joint borrower |

| Main purpose | Backstop for the debt | Jointly take on the debt |

| Debt responsibility | Responsible if borrower defaults; exact wording depends on documents | Equally responsible for repayment |

| Account access / disclosure | Not always the same as a joint borrower | Joint borrower disclosure rights generally apply with federally regulated institutions |

| Title / ownership | Often not on title, but lender and legal structure matter | May be on title or otherwise part of the borrowing structure, depending on the deal |

| Best fit | Family support where lender accepts a guarantee | Files needing stronger joint-borrower support |

This table is a practical summary, not legal advice. The same lender may structure two similar files differently depending on province, product, and insurer requirements.

What Should Homebuyers and Helpers Do Before Signing?

Before anyone signs, both sides should understand the full payment, the qualification rules, the title plan, and the exit strategy.

A safe process usually looks like this:

- Confirm whether the lender is proposing a guarantor or joint-borrower structure

- Ask how that structure affects approval, title, disclosure, and future refinancing

- Review whether the application is insured or uninsured

- Run the file through current stress-test rules

- Check the down-payment and insured-mortgage rules that apply to the purchase price

- Make sure the helper understands they may be fully on the hook if payments are missed

- Consider independent legal advice, especially for guarantees

- Discuss the exit plan before closing, not years later

Decision checkpoint: If the helper does not fully understand the repayment risk and exit plan, the conversation is not finished yet.

Why Professional Help Matters

This is one of those mortgage topics where casual language causes real problems. Families often say “guarantor” when the lender is actually setting up a joint-borrower file, or they assume a guarantor is just a formality when the legal exposure is much larger.

A mortgage professional can help you:

- Clarify whether the lender will accept a guarantee structure at all

- Compare a guarantor setup with a co-signer setup

- Explain how the stress test and debt ratios still apply

- Identify whether insured-mortgage rules affect the file

- Flag when legal advice is especially important

At Pegasus, the goal is not just to get the deal approved. It is to help you understand what structure makes sense and what risks each person is taking on.

Example Scenario

A first-time buyer wanted a parent to “guarantee” the mortgage, but the lender was more comfortable treating the parent as a joint borrower. That changed the discussion from simple family support to a much more serious debt obligation. Once everyone understood the difference, the family could decide whether the structure still made sense.

Common Mistakes Buyers Make

Most problems happen when families treat these labels casually.

Common mistakes include:

- Using the terms interchangeably

- Assuming help removes the stress test

- Ignoring debt-ratio limits

- Not asking about title and ownership

- Skipping legal advice for the helper

- Thinking federal rule changes made approval easy

- Having no exit plan for removing the helper later

Key takeaway: The biggest mistake is not the structure itself. It is signing before everyone understands what the structure really means.

FAQ

Can a guarantor help you get approved for a mortgage in Canada?

Sometimes, yes. A guarantor may strengthen the file if the lender and insurer accept that structure and the added support improves the application’s overall strength.

Is a co-signer equally responsible for the mortgage?

Yes. FCAC says a joint borrower, also referred to as co-signing, becomes equally responsible for repaying the unpaid balance.

Is a guarantor the same as being on title?

Not necessarily. A guarantor often supports the loan without taking the same borrower or ownership role, but the exact title structure depends on the lender and legal documents.

Does a guarantor remove the mortgage stress test?

No. Current qualifying-rate rules still apply.

What credit and debt rules still matter on an insured file?

CMHC says at least one borrower or guarantor must have a minimum credit score of 600. It also points to maximum insured debt-service thresholds of 39% GDS and 44% TDS.

What changed recently that homebuyers should still know in 2026?

The insured-mortgage cap rose to $1.5 million effective December 15, 2024, and 30-year insured amortizations became available to all first-time homebuyers and all buyers of new builds.

Should parents get independent legal advice before guaranteeing a mortgage?

That is often wise. Sagen’s underwriting materials specifically note that lenders should consider provincial law and allow guarantors the opportunity to receive independent legal advice.

Final Thoughts

The key takeaway is simple: a guarantor and a co-signer can both help a mortgage application, but they do not mean the same thing and they do not create the same legal position.

For many Canadian buyers in 2026, the best path is not asking which label sounds better. It is asking:

- Which structure will the lender actually approve?

- How will the helper’s risk be documented?

- Will the mortgage still work under today’s qualification rules?

- What is the plan for removing the helper later?

Do not rely on casual language from friends or online forums when the legal and financial consequences are this serious. Review the mortgage structure, title plan, and exit strategy before anyone signs.

If you are deciding between a guarantor and a co-signer, speak with a mortgage professional early so you can improve approval odds without creating avoidable surprises later.

Sources & References

- https://www.canada.ca/en/financial-consumer-agency/services/rights-responsibilities/rights-credit-loans/rights-joint-borrower-disclosure.html

- https://www.canada.ca/en/financial-consumer-agency/services/credit-cards/joint-credit-card.html

- https://www.canada.ca/en/financial-consumer-agency/services/rights-responsibilities/rights-mortgages.html

- https://www.osfi-bsif.gc.ca/en/supervision/financial-institutions/banks/minimum-qualifying-rate-uninsured-mortgages

- https://www.osfi-bsif.gc.ca/en/guidance/guidance-library/infosheet-residential-mortgage-underwriting-practices-procedures-guideline-b-20

- https://www.cmhc-schl.gc.ca/professionals/project-funding-and-mortgage-financing/mortgage-loan-insurance/mortgage-loan-insurance-homeownership-programs/purchase

- https://www.cmhc-schl.gc.ca/professionals/project-funding-and-mortgage-financing/mortgage-loan-insurance/calculating-gds-tds

- https://www.cmhc-schl.gc.ca/professionals/project-funding-and-mortgage-financing/mortgage-loan-insurance/mortgage-loan-insurance-homeownership-programs/home-start

- https://www.canada.ca/en/financial-consumer-agency/services/mortgages/down-payment.html

- https://www.canada.ca/en/department-finance/news/2024/09/government-announces-mortgage-reform-details-to-ensure-canadians-can-access-lower-monthly-mortgage-payments-by-december-15.html

- https://www.canada.ca/en/department-finance/news/2024/12/boldest-mortgage-reforms-in-decades-come-into-force-today.html

- https://www.canada.ca/en/department-finance/news/2024/09/delivering-the-boldest-mortgage-reforms-in-decades.html

- https://www.sagen.ca/ups/covenant-underwriting/