A sole proprietor in Canada may qualify for a mortgage in 2026, but approval usually comes down to three things: clear income documentation, manageable debt ratios, and passing the mortgage stress test. For many buyers, the challenge is not earning income. It is proving income in a format a lender can underwrite with confidence.

Buying a home as a sole proprietor can feel frustrating. Your business may be steady, your clients may pay on time, and your cash flow may look healthy. But mortgage approval often depends on what shows up on your tax return, how consistent that income looks, and whether your file is easy to verify.

This guide explains how lenders typically assess sole proprietor income, how tax choices can affect borrowing power, and which practical steps may improve your approval odds before you make an offer.

Need a quick gut check before you shop? Start with a mortgage pre-approval and a document review so you know your real budget, not just your hopeful one.

Quick Start: Pick Your Path

- Newly self-employed? Focus first on documentation depth and lender fit.

- Have two or more years of filed returns? Focus on declared income, debt ratios, and down payment strategy.

- Claim many business deductions? Focus on how net income affects borrowing power.

- Choosing between staying a sole proprietor or incorporating? Focus on income structure, liability, and long-term planning.

- Planning to buy soon? Focus on pre-approval, document cleanup, and a realistic price range.

Why Is Buying a Home Harder for a Sole Proprietor?

A sole proprietor often faces more mortgage scrutiny because income can fluctuate, tax filings may show lower net income after deductions, and lenders need proof that income is stable and sustainable over time. Self-employment itself is not the problem. The challenge is proving repayment capacity in a way the lender can measure clearly.

A sole proprietor is an unincorporated business owner who reports business income on a personal tax return. That creates a different approval path than a salaried employee with predictable pay stubs and T4 income.

For mortgage purposes, lenders usually care less about how busy you are and more about whether your income story is:

- Documented

- Consistent

- Reasonable after expenses

- Strong enough to pass debt-ratio and stress-test rules

takeaway: A healthy business does not always translate into strong qualifying income on paper.

What Income Do Lenders Usually Use for a Sole Proprietor?

For a sole proprietor, lenders often look closely at filed tax documents and supporting records. In many cases, they focus more on net business income than gross revenue, because net income reflects what remains after eligible business expenses.

That distinction matters.

- Gross revenue is your top-line business sales.

- Net income is what remains after eligible expenses are deducted.

You can have strong revenue and still show modest income for mortgage qualification purposes.

Most strong files include:

- Personal tax returns

- Notices of Assessment

- T2125 details

- CRA proof of income statement

- Business bank statements

- Accountant-prepared financials, when available

A good rule to remember is this: strong revenue is not the same as strong qualifying income. Lenders generally need income they can document, defend, and calculate consistently.

Another important point: a legitimate tax deduction may lower your tax bill, but it may also reduce the income a lender uses to approve your mortgage. That does not mean you should avoid valid deductions. It means tax planning and mortgage planning should work together.

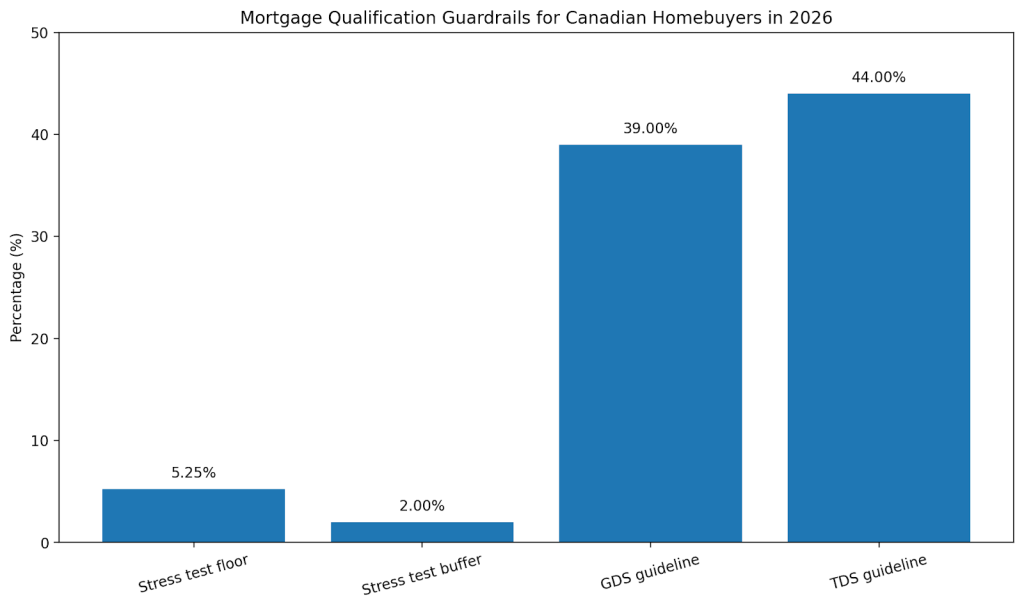

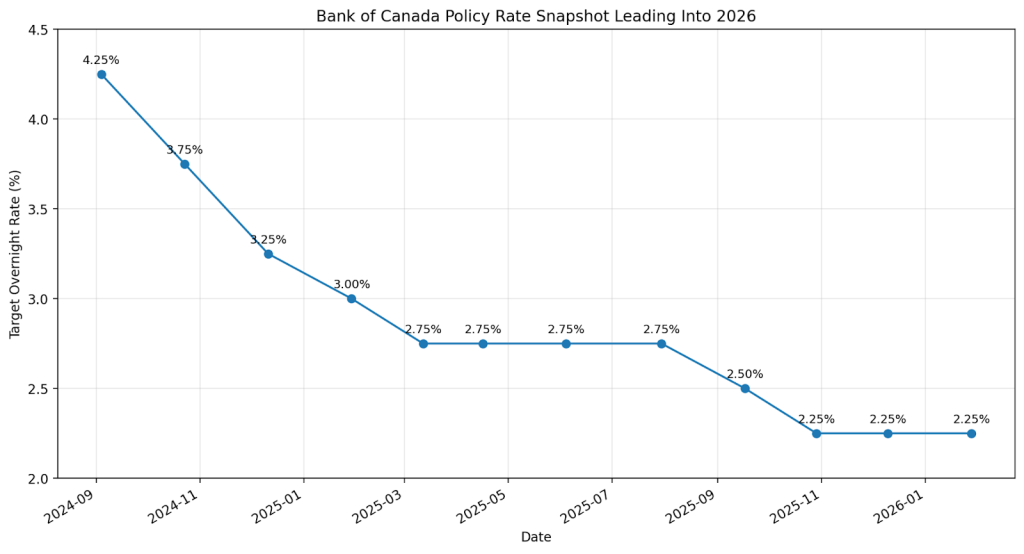

How Does the Stress Test Affect Sole Proprietor Homebuyers in 2026?

The mortgage stress test can reduce borrowing power, even when your actual contract payment looks manageable. At federally regulated lenders, borrowers generally need to qualify at the higher of the minimum benchmark rate or the contract rate plus a buffer.

In practice, that means your application is judged using a higher payment than the one you may actually make. This can shrink your maximum purchase price, especially if your income varies or your other debts are already stretching your ratios.

Here is where the math usually gets tight:

- Higher qualifying rates increase your tested payment

- Higher tested payments push up your housing ratio

- Existing debts can push your total debt ratio too high

- Variable or lightly documented income can reduce lender comfort

For example, a sole proprietor with solid cash flow may still qualify for less than expected if they carry credit card balances, a vehicle loan, or a line of credit alongside housing costs.

Decision checkpoint: If your buying power looks tighter than expected, consider reducing revolving debt or adjusting your target price before you start bidding.

Which Documents Matter Most?

For sole proprietor borrowers, strong documentation reduces ambiguity. The cleaner your file, the easier it is for an underwriter to verify your income and move your application forward.

The strongest package usually includes:

- Two years of filed personal tax returns

- Two years of Notices of Assessment

- T2125 details

- CRA proof of income statement

- Business bank statements

- Accountant-prepared financials, if available

- Government-issued ID

- Down payment proof

- A clear summary of current debts and obligations

Organized records matter because they help show that your income is not only real, but stable and understandable. Separate business and personal accounts can also make the file easier to review.

Key takeaway: A clean file can improve lender confidence and reduce approval friction.

What Strategies May Help a Sole Proprietor Qualify More Smoothly?

The most effective mortgage strategies for sole proprietors usually come down to earlier planning, clearer records, better ratio management, and the right lender fit.

Here are some of the most practical moves:

- Show consistent reported income. If you expect to buy soon, speak with your accountant before filing so you understand how deductions may affect qualification.

- Keep business and personal finances separate. Cleaner records make it easier to support income and expenses.

- Reduce other debts before applying. Paying down credit cards, lines of credit, or auto loans may improve affordability faster than many buyers expect.

- Build a stronger down payment. A larger down payment may reduce pressure on debt ratios and improve lender flexibility.

- Use a broker early. The right lender path may depend on your business history, income pattern, and documentation strength.

There is rarely one magic fix. Preparation usually matters more than last-minute tactics.

Why Professional Help Matters

A generic affordability calculator can only go so far. It will not tell you how a lender may interpret your income trend, how deductions could affect your file, or whether a different lender path might suit a self-employed borrower better.

That is where tailored guidance can make a real difference. A mortgage professional can help you:

- Review how your income may be presented

- Spot debt-ratio issues before they become deal killers

- Compare realistic lender options based on your file

- Time your pre-approval around tax filing and down payment readiness

At Pegasus, the goal is not to guess what might work. It is to build a cleaner, more lender-ready application based on your actual numbers and timeline.

Example Scenario

A sole proprietor with solid revenue wanted to buy within three months. On the surface, the business looked strong. But the borrower had high revolving debt and recent deductions that lowered reported net income.

The better move was not to rush an offer. It was to tighten records, reduce some debt, and review lender fit before shopping. The result was a more realistic budget and a smoother path through underwriting.

Does Sole Proprietor vs. Corporation Matter for a Homebuyer?

Yes. Your business structure can affect how income is reported, how lenders interpret earnings, and how much flexibility you have when planning compensation.

A sole proprietor reports business income on a personal return. An incorporated borrower usually works within a separate corporate tax structure and may pay themselves through salary, dividends, or a mix of both.

That does not mean incorporation is automatically better for mortgage approval. It means the income story changes.

| Feature | Sole Proprietor | Incorporated Borrower |

| Core tax reporting | Personal return with business reporting | Corporate filing plus personal income reporting |

| Income lenders often review | Net business income on personal returns | Salary, dividends, and other documented personal income |

| Simplicity | Usually simpler | Usually more complex |

| Common mortgage planning issue | Write-offs can reduce net income | Compensation structure can affect provable income |

| Best fit | Straightforward operations | Longer-term structure and planning needs |

Decision checkpoint: If you are weighing incorporation mainly for mortgage reasons, treat it as a tax, legal, and mortgage planning decision together, not a quick fix.

A Practical Roadmap Before You Start House Hunting

A strong sole proprietor mortgage plan usually starts months before you make an offer.

Follow this sequence:

- Review your last two years of filed returns and Notices of Assessment

- Pull your CRA proof of income statement

- Reconcile business records, receipts, and bank statements

- Estimate affordability using realistic stress-test and debt-ratio assumptions

- Pay down revolving debt where possible

- Confirm your down payment source and closing-cost reserves

- Speak with your accountant about timing if a home purchase is coming up

- Get broker guidance before shopping, not after

Common Mistakes Sole Proprietor Buyers Make

Most self-employed mortgage problems come from timing, documentation gaps, and misunderstanding how lenders read tax returns.

Common mistakes include:

- Writing off aggressively right before a mortgage application

- Shopping before checking debt ratios

- Mixing business and personal finances

- Applying with incomplete documents

- Assuming strong revenue equals strong approval odds

- Waiting too long to talk to a broker

- Ignoring business age and income consistency

Key takeaway: Most approval problems are easier to fix before you make an offer than after you are under deadline pressure.

FAQ

Can a sole proprietor get a mortgage in Canada in 2026?

Yes. A sole proprietor may qualify, but lenders usually want strong income documentation, acceptable debt ratios, and a successful stress-test result. Self-employment is not a disqualifier by itself.

Do lenders use gross sales or net income?

Many lenders focus more on net income than gross sales because net income reflects what remains after expenses. That is why tax returns and business reporting details matter so much.

How many years of self-employment history do I usually need?

Two years is a common benchmark for many self-employed files, although some borrowers may still have options when other factors are strong.

What documents should I prepare first?

Start with your personal tax returns, Notices of Assessment, T2125 details, CRA proof of income statement, and organized business records.

Does the mortgage stress test still matter in 2026?

Yes. It can still reduce buying power because borrowers at federally regulated lenders are generally qualified using a higher benchmark rate.

Can tax planning hurt mortgage approval?

It can affect qualification. Legitimate deductions may lower taxable income, and lower taxable income may reduce the amount some lenders are willing to use.

Is incorporation always better for getting a mortgage?

No. It changes how income is reported and planned, but it is not automatically better for every borrower.

Final Thoughts

The eye-opening part for many buyers is this: the mortgage process often rewards clarity more than hustle. You may earn well, but approval usually depends on whether your income looks documented, stable, and stress-test ready.

That is why the smartest 2026 strategy is usually simple:

- Plan earlier

- Keep cleaner records

- Understand how tax choices affect reported income

- Test affordability before you shop

- Match your application to the right lender path from the start

If you want a realistic path to approval, stop guessing and speak with a Pegasus mortgage professional before you make an offer. A quick review can help you understand your documentation gaps, likely lender paths, and next best steps.