A mortgage can look affordable on paper and still put real pressure on your budget.

That usually happens when buyers focus on the interest rate and monthly payment, but overlook the costs wrapped around the loan. Some hit before closing. Others appear only if you refinance, sell, or switch lenders. A few are tucked into lender disclosures that borrowers do not read closely until it is too late.

In 2026, mortgage affordability is about more than the rate you are quoted. It is about how much cash you need up front, how flexible the mortgage is if your plans change, and how rules like the stress test shape what you can actually carry. This guide breaks down the hidden fees Canadians should budget for, what they mean in plain English, and what questions to ask before you sign.

Looking for the next step? See our mortgage pre-approval guide for Ontario buyers, fixed vs. variable mortgage guide for Canadians, and mortgage renewal checklist in Canada.

What hidden mortgage costs affect affordability in 2026?

The biggest hidden costs are usually:

- closing costs

- land transfer tax

- mortgage default insurance

- provincial sales tax on that insurance in some provinces

- legal fees

- appraisal fees

- discharge fees

- prepayment penalties

These costs affect either your upfront cash requirement, your monthly carrying cost, or the price of changing your mortgage later.

A mortgage is only truly affordable if you can handle both the payment and the non-rate costs around it.

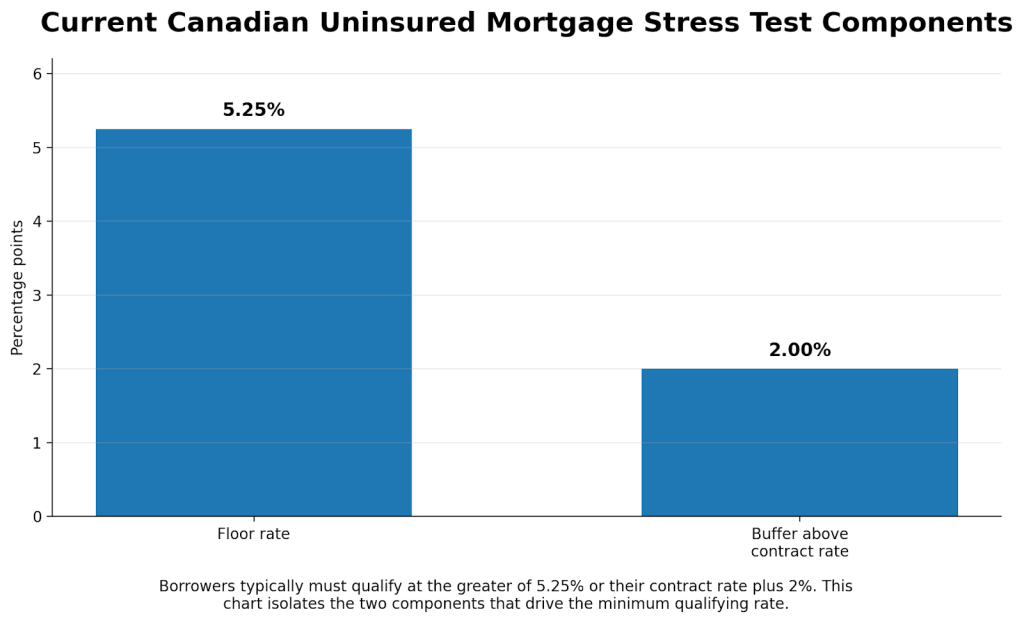

For many uninsured mortgages at federally regulated lenders, borrowers still have to qualify at the greater of 5.25% or the contract rate plus 2%, under the federal minimum qualifying rate, also known as the stress test. That can reduce how much you qualify for before you even start counting fees. As the Office of the Superintendent of Financial Institutions explains, this rule is meant to test whether borrowers could still carry the mortgage if conditions worsen.

A prepayment penalty is the fee a lender may charge if you pay off too much of a mortgage early, refinance before maturity, transfer it to another lender before term-end, or break the contract when you sell. The Financial Consumer Agency of Canada notes that these penalties can cost thousands of dollars.

Key takeaway: A mortgage that looks affordable at signing can become expensive to exit.

Which upfront closing costs surprise buyers most in Ontario?

In Ontario, buyers often budget for the down payment and forget that closing day needs separate cash.

The biggest surprises are usually:

- land transfer tax

- legal fees

- title-related costs

- tax adjustments

- appraisal-related lender costs

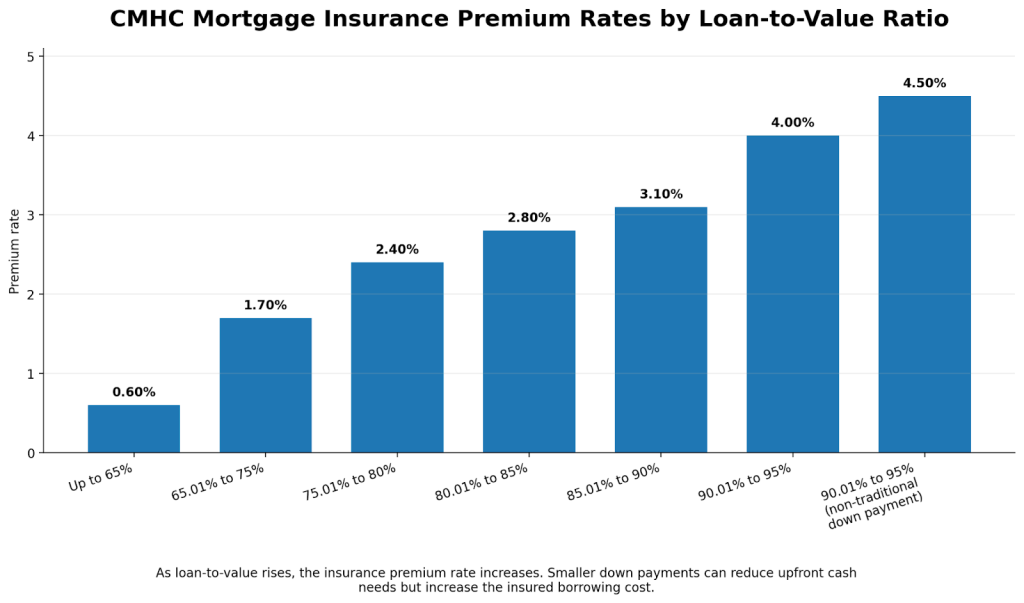

- mortgage default insurance if the down payment is under 20%

- Ontario provincial sales tax on the insurance premium

The FCAC mortgage qualifier guidance tells borrowers to keep extra money available for closing costs, lawyers’ fees, land transfer taxes, tax adjustments, and moving expenses. That is a good reminder that affordability is also about liquidity, not just monthly payment.

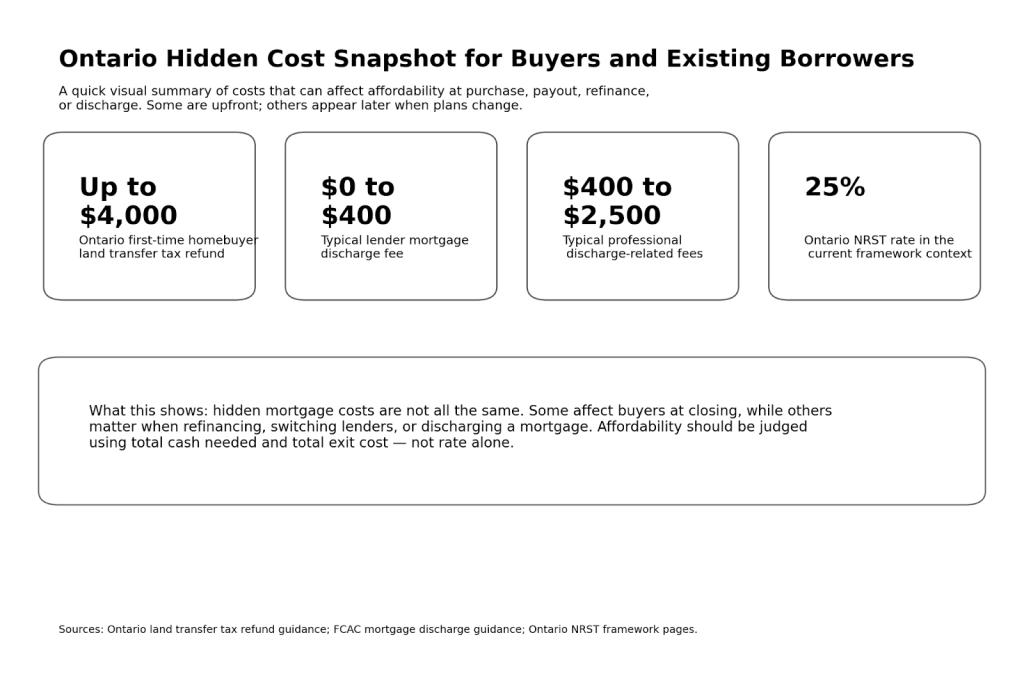

For Ontario buyers, land transfer tax is often the largest non-rate shock. The Ontario Ministry of Finance explains that land transfer tax applies on registrations and dispositions of land. Eligible first-time homebuyers may qualify for a refund of up to $4,000, according to the province’s first-time homebuyer refund guidance.

If your down payment is under 20%, mortgage default insurance may apply. CMHC says the premium is calculated as a percentage of the loan and depends on the size of your down payment. In Ontario, the provincial sales tax on that premium is generally paid out of pocket at closing rather than added to the mortgage.

If your down payment is under 20%, budget for both the insurance premium and the tax tied to it.

How much can it cost to break a mortgage early in Canada?

This is where many affordability plans fall apart.

Breaking a mortgage early can trigger more than one charge. For a closed mortgage, the FCAC says borrowers may face:

- a prepayment penalty

- administration fees

- appraisal fees

- reinvestment fees

- a mortgage discharge fee

- repayment of mortgage cash back, if the original deal included it

That total can easily reach the thousands.

A mortgage discharge is the legal process of removing the lender’s charge from your property title after the mortgage is paid off or replaced. The FCAC’s mortgage discharge guidance says discharge fees can range from no charge to $400 depending on the lender and province, while related legal or notarial fees are often much higher.

That is why borrowers should never judge a refinance or sale decision on rate alone. The better question is whether the savings outweigh the full exit cost.

Decision checkpoint: If you may move, refinance, or upgrade within a few years, compare the break cost before you choose the lower headline rate.

How do fixed and variable mortgage penalties compare?

Fixed and variable mortgages are not just different because of payment style. They can also be very different when it is time to leave early.

Here is the practical difference:

- Variable-rate closed mortgages often use a simpler penalty calculation, commonly three months’ interest.

- Fixed-rate closed mortgages can cost much more to break because lenders may charge the greater of three months’ interest or an interest rate differential calculation.

- Variable penalties are usually easier to estimate.

- Fixed penalties can be much harder to predict, especially when rates have changed since you signed.

RBC’s prepayment calculator guidance explains that for fixed-rate closed mortgages, the charge is often the greater of three months’ interest or an interest rate differential amount. For variable-rate mortgages, it is commonly three months’ interest. The Bank of Canada also notes that many lenders use interest rate differential penalties during the first five years, which can leave borrowers paying close to the interest the lender expected to earn.

That does not make fixed-rate mortgages bad. It means borrowers should compare flexibility cost, not just the starting payment.

If payment stability matters most, fixed may still fit. If flexibility matters most, penalty structure deserves equal attention.

What refinance and switch costs should borrowers expect?

A straight switch at renewal and a refinance are not the same thing.

A straight switch may involve few or no fees if you keep the same balance and amortization. A refinance is different. It may involve:

- legal fees

- appraisal fees

- lender setup costs

- discharge fees

- a new qualification process

- a prepayment penalty if you leave before maturity

The OSFI guidance says the minimum qualifying rate is not expected to apply to uninsured straight switches at renewal between federally regulated lenders when there is no increase to the loan amount or amortization period.

That can make switching easier for some borrowers. But once you change the balance, extend the amortization, or pull out equity, the transaction may become a refinance instead of a simple switch.

CIBC notes that many switches at renewal can be done without legal or setup fees, while refinancing may bring additional legal and appraisal costs.

Before you compare offers, confirm whether you are doing a straight switch or a refinance. That one detail can change both cost and qualification.

Which 2026 mortgage rules change affordability calculations?

In 2026, affordability is shaped by more than rates. It is also shaped by underwriting and insurance rules.

The main rules borrowers should know are:

- the federal mortgage stress test

- insured mortgage eligibility up to a $1.5 million home price cap

- broader access to 30-year insured amortizations for first-time homebuyers and buyers of new builds

The stress test still matters because it affects how much you can qualify for, even if the real payment looks manageable.

The insured mortgage cap increased to $1.5 million, and the federal government also expanded access to 30-year insured amortizations for all first-time homebuyers and all buyers of new builds. The Department of Finance Canada describes both changes as part of the current mortgage rule framework.

Longer amortization can lower the monthly payment, but it usually increases the total interest paid over time. Lower monthly cost does not always mean lower total cost.

Bottom line: Rule changes may improve monthly cash flow or qualification, but they do not erase fee risk or long-term cost.

Why professional help still matters

Mortgage calculators are useful, but they do not always capture the details that shape real affordability.

They usually do not tell you:

- how a lender calculates fixed-rate penalties

- whether your switch qualifies as a straight transfer or a refinance

- how much closing-day cash you need after taxes and adjustments

- whether a slightly higher rate comes with more flexible prepayment terms

That is where a mortgage professional can add value. A good review should help you compare not only payment size, but also closing costs, penalty exposure, flexibility, and the total cost of leaving early.

A mortgage that fits your budget today should also fit your life six months, two years, and five years from now.

Step-by-step roadmap before you sign or switch

Start with the payment you can comfortably afford, not the maximum a calculator says you can qualify for.

Then work through this checklist:

- Ask for the total cash needed to close, including legal fees, land transfer tax, tax adjustments, title-related costs, and insurance-related taxes.

- Ask whether the mortgage is open or closed.

- Ask for the exact prepayment penalty formula, especially on a fixed-rate mortgage.

- If you may move or refinance within a few years, compare the cost to break alongside the interest rate.

- Confirm whether the transaction is a straight switch or a refinance.

- If your down payment is under 20%, ask how much the mortgage insurance premium is and how much Ontario PST applies at closing.

- Review whether a 30-year amortization helps enough on monthly cash flow to justify the higher long-term interest cost.

- Keep a reserve for unexpected costs after closing.

Common mistakes borrowers make

- Comparing mortgages by rate alone

- Ignoring closing-day cash needs

- Assuming all switches are free

- Choosing fixed without asking about the penalty formula

- Forgetting Ontario PST on mortgage insurance

- Treating a lower monthly payment as a lower total cost

- Skipping the prepayment privilege details

FAQ

What is the most overlooked mortgage cost in Canada?

For many borrowers, it is the total cost of leaving early. That may include a prepayment penalty, discharge fee, legal fees, appraisal fees, and other administration charges, not just the monthly payment at origination.

Are mortgage penalties always charged when you break a mortgage?

No. Open mortgages generally can be broken without a prepayment penalty, while closed mortgages normally involve one. Your exact result depends on your contract and lender terms.

Is a fixed-rate mortgage penalty usually higher than a variable-rate penalty?

Often, yes. Variable-rate penalties are commonly based on three months’ interest, while fixed-rate penalties may use the greater of three months’ interest or an interest rate differential calculation.

Do I pay Ontario land transfer tax in cash at closing?

Usually, yes. Ontario land transfer tax is a closing cost that is separate from your regular mortgage payment. Eligible first-time homebuyers may qualify for a refund of up to $4,000.

Can mortgage insurance affect affordability even if it is added to the mortgage?

Yes. If the premium is added to the loan, it increases the amount you borrow and can raise your payments over time. In Ontario, the provincial sales tax on that premium is generally not added to the loan amount.

Does switching lenders at renewal trigger the stress test?

Not always. For uninsured straight switches at renewal between federally regulated lenders, the minimum qualifying rate is not expected to apply when there is no increase to the loan amount or amortization period.

Do 30-year amortizations make a mortgage more affordable?

They may lower the monthly payment, which can help with cash flow and qualification. But they also usually increase the total interest paid over time.

The bottom line on mortgage affordability

Mortgage affordability in 2026 is about more than qualifying for a loan. It is about understanding the full cost of getting in, carrying the mortgage, and getting out if your plans change.

The good news is that these costs are usually knowable in advance. When you ask better questions, you can compare mortgages more clearly, avoid common surprises, and make a decision that fits both your budget and your flexibility needs.

Stop guessing. Review the all-in cost before you sign, renew, refinance, or switch. Bring your mortgage quote, current balance, amortization, and any penalty estimate so you can compare the real numbers side by side.

Disclaimer: This article is general information, not legal, tax, or financial advice. Mortgage costs vary by lender, province, property type, and borrower profile. Rules and fees may change, and your mortgage commitment and disclosure documents should always control.

mortgage prepayment penalty Canada

Sources & References

- Office of the Superintendent of Financial Institutions — Minimum qualifying rate for uninsured mortgages https://www.osfi-bsif.gc.ca/en/supervision/financial-institutions/banks/minimum-qualifying-rate-uninsured-mortgages

- Financial Consumer Agency of Canada — Mortgage fees: Prepayment penalties

https://www.canada.ca/en/financial-consumer-agency/services/mortgages/reduce-prepayment-penalties.html - Financial Consumer Agency of Canada — Breaking your mortgage contract

https://www.canada.ca/en/financial-consumer-agency/services/mortgages/break-mortgage-contract.html - Financial Consumer Agency of Canada — Discharging a mortgage

https://www.canada.ca/en/financial-consumer-agency/services/mortgages/mortgage-discharge.html - Financial Consumer Agency of Canada — Mortgage prepayment: know your rights

https://www.canada.ca/en/financial-consumer-agency/services/rights-responsibilities/rights-mortgages/rights-prepayments.html - Financial Consumer Agency of Canada — Mortgage qualifier tool / applying guidance

https://itools-ioutils.fcac-acfc.gc.ca/MQ-HQ/MQ-EAPH-eng.aspx - Canada Mortgage and Housing Corporation — CMHC Mortgage Loan Insurance Cost

https://www.cmhc-schl.gc.ca/consumers/home-buying/mortgage-loan-insurance-for-consumers/cmhc-mortgage-loan-insurance-cost - Canada Mortgage and Housing Corporation — What is mortgage loan insurance? https://www.cmhc-schl.gc.ca/consumers/home-buying/mortgage-loan-insurance-for-consumers/what-is-mortgage-loan-insurance

- Canada Mortgage and Housing Corporation — Mortgage calculator

https://www.cmhc-schl.gc.ca/consumers/home-buying/calculators/mortgage-calculator - Department of Finance Canada — Mortgage reform details https://www.canada.ca/en/department-finance/news/2024/09/government-announces-mortgage-reform-details-to-ensure-canadians-can-access-lower-monthly-mortgage-payments-by-december-15.html

- Department of Finance Canada — Mortgage reforms in force

https://www.canada.ca/en/department-finance/news/2024/12/boldest-mortgage-reforms-in-decades-come-into-force-today.html - Ontario Ministry of Finance — Calculating land transfer tax

https://www.ontario.ca/document/land-transfer-tax/calculating-land-transfer-tax - Ontario Ministry of Finance — Refunds of land transfer tax, including first-time homebuyer refund

https://www.ontario.ca/document/land-transfer-tax/refunds-land-transfer-tax-including-non-resident-speculation-tax-and - Ontario Ministry of Finance — Non-Resident Speculation Tax collected

https://www.ontario.ca/document/non-resident-speculation-tax/non-resident-speculation-tax-collected - RBC Royal Bank — Mortgage prepayment charge calculator guidance https://www.rbcroyalbank.com/cgi-bin/mortgage/tools/prepayment/prepayment-charge-calculator.cgi

- CIBC — What are mortgage prepayment charges?

https://www.cibc.com/en/personal-banking/mortgages/resource-centre/prepayment.html - CIBC — How to switch your mortgage provider

https://www.cibc.com/en/personal-banking/mortgages/switch-mortgage.html - Bank of Canada — Canada’s mortgage market: A question of balance

https://www.bankofcanada.ca/2024/11/canadas-mortgage-market-a-question-of-balance/