Buying your first place can feel like trying to hit a moving target—home prices, down payments, closing costs, and those “surprise” fees that show up right when you’re already stretched.

If you’re one of the many first time homebuyers aiming for 2026, here’s the good news: Canada’s system has more levers than most people realize. The even better news? The biggest savings usually come from a few predictable moves—starting early, picking the right accounts, and avoiding the small mistakes that quietly cost thousands.

This guide gives you a practical roadmap for first time homebuyers in Canada:

Quick start: pick your path

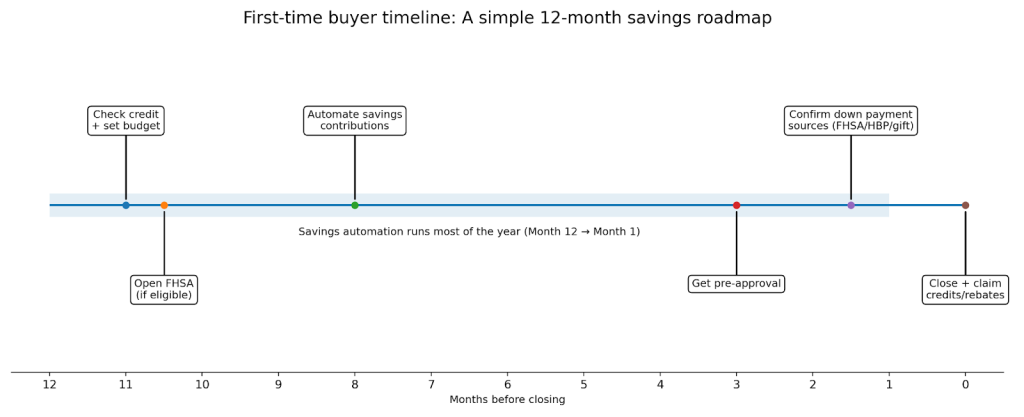

Buying in the next 0–3 months

- Get a pre-approval and set your all-in budget (payment + property taxes + condo fees + utilities)

- Confirm down payment sources (savings, FHSA, RRSP HBP, gift)

- Start collecting documents now (employment, income, IDs, bank history)

Buying in the next 3–12 months

- Open and fund an FHSA if you qualify

- Decide whether the HBP fits your plan (and your budget)

- Build a closing-cost buffer (legal fees, land transfer tax, inspection, moving)

Buying in 12+ months

- Automate monthly savings (no willpower required)

- Improve credit health (reduce balances, avoid new debt)

- Track programs in your province/city (rebates and transfer-tax relief vary widely)

The “real” cost of buying your first home

Most first-time buyers focus on the down payment (understandably). But what keeps you comfortable is the full cost of ownership:

- Closing costs: legal fees, title insurance, appraisal (if required), inspection

- Land transfer tax / property transfer tax: varies by province (and sometimes city)

- Move-in costs: moving, utilities setup, basics, small repairs

- Ongoing costs: property taxes, condo fees (if applicable), home insurance

For most first time homebuyers, the strongest 2026 savings strategy is stacking:

- tax-advantaged saving (FHSA),

- smart withdrawals (HBP only if it truly fits),

- credits you claim after closing (Home buyers’ amount), and

- location-based programs (provincial + municipal rebates).

The biggest savings lever: the First Home Savings Account (FHSA)

If you qualify, the FHSA is one of the most powerful tools for first time homebuyers because it’s designed specifically for a first purchase.

Why the FHSA matters

The FHSA blends what people like about other accounts:

- contributions are tax-deductible (like an RRSP)

- growth inside the account is tax-sheltered

- a qualifying withdrawal for a first home can be tax-free

Key FHSA basics to know in 2026 (high level)

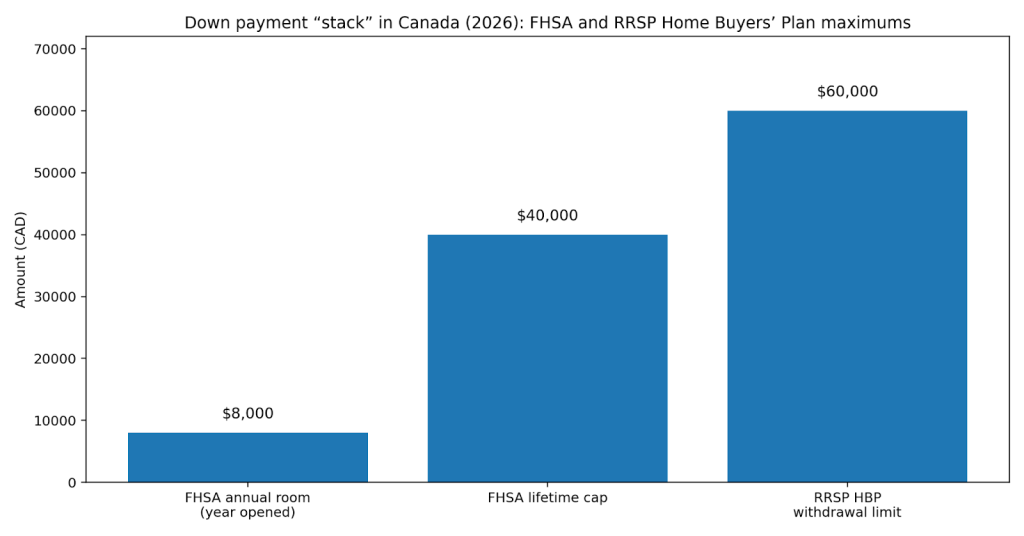

- Annual contribution room is generally $8,000 in the year you open your first FHSA.

- There’s a lifetime contribution limit of $40,000.

- “First-time home buyer” eligibility for a qualifying withdrawal has its own test (often described as: you didn’t live in a home you or your spouse/partner owned in the current year—with a limited exception—or the prior four calendar years).

What this means for you

If you’re buying as a couple and both qualify, each person may be able to build their own FHSA strategy—meaning you may be able to accelerate the down payment plan. The move is starting early so you don’t waste contribution room.

The Home Buyers’ Plan (HBP): useful, but only when it fits your plan

The Home Buyers’ Plan (HBP) lets eligible buyers withdraw from their RRSP to buy or build a qualifying home.

The part most people miss: repayment pressure

The HBP isn’t “free money.” It creates a repayment obligation over time. And while there has been temporary repayment relief for certain first withdrawals in recent years, the key point for first time homebuyers is this:

If your monthly budget will already feel tight after closing, an HBP repayment schedule can turn “helpful” into stressful fast.

When HBP can be a win

HBP tends to work best when:

- your RRSP is already funded (you’re not scrambling at the last minute)

- you can realistically repay it later

- you’re using it to reduce high-interest borrowing—not to stretch into an uncomfortable price

When HBP can backfire

Be cautious if:

- your post-closing budget is tight (repayments become painful)

- you’re relying on HBP to “force” a purchase price that doesn’t really fit

- you’re draining retirement savings without a replacement plan

Homebuyer tax credits in Canada (don’t forget to claim them)

Some savings don’t show up until tax time.

Home buyers’ amount (first-time homebuyers’ tax credit)

The federal home buyers’ amount is a non-refundable tax credit. Translation: it can reduce the tax you owe, but it won’t create a refund if you don’t have tax payable.

Practical tip: Keep purchase documents organized (closing statement, agreements, proof of occupancy). It makes claiming easier and reduces stress if you’re ever asked to support the claim.

Buying a new build in 2026? Watch GST/HST rebates closely

If you’re buying newly built or substantially renovated housing, rebates can materially reduce your out-of-pocket costs—but the rules are specific.

Existing GST/HST new housing rebate

There’s an established GST/HST new housing rebate framework, including rules around what qualifies (new construction, substantial renovations, and other scenarios).

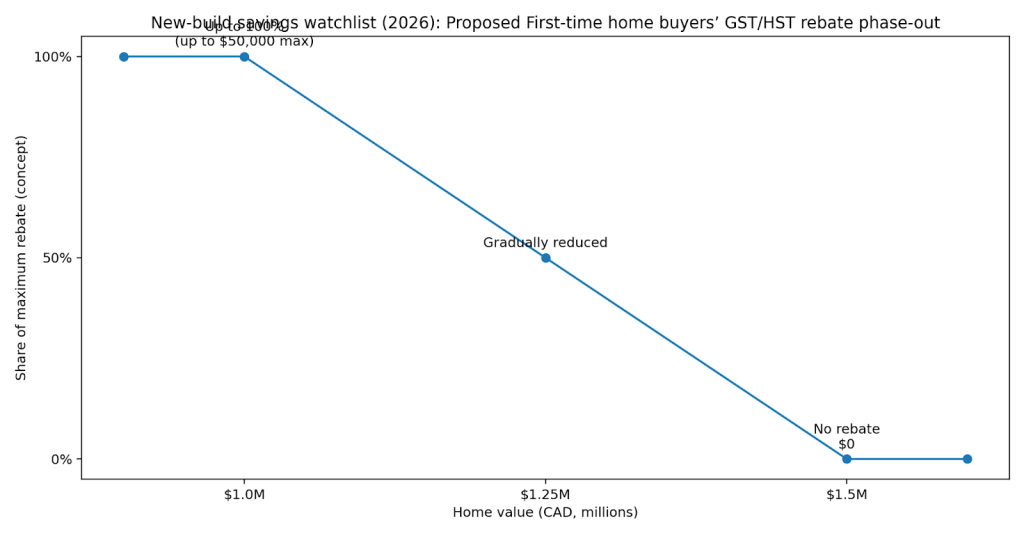

GST relief for first-time buyers on new homes (recent policy)

The federal government announced GST relief for first-time buyers on new homes (with full GST relief up to a value threshold and a phase-out range above it). Because eligibility and implementation details matter, treat this as a “check the official rules before you act” item—especially if you’re signing an agreement with a builder.

Provincial (and city) programs can change your costs dramatically

This is where first time homebuyers can save (or overspend) based purely on location.

Examples worth researching before you write an offer

- British Columbia: The first-time home buyers’ program can reduce or eliminate property transfer tax if you qualify.

- Ontario: First-time homebuyers may qualify for a land transfer tax refund up to a set maximum.

- Toronto: There’s a separate Municipal Land Transfer Tax (MLTT) rebate for eligible first-time purchasers.

Before you go offer-shopping, look up:

- your province’s transfer tax rules

- any city-level rebates (Toronto is the classic example)

- occupancy requirements (many programs require you to move in within a set period)

Common mistakes that cost first-time buyers real money

- Waiting too long to open an FHSA. Delaying can mean missing contribution room you could have used.

- Assuming “first-time buyer” means the same thing everywhere. Definitions can differ by program.

- Using the HBP without a repayment plan. It can be useful, but repayment timing rules matter.

- Forgetting transfer taxes and closing costs. These can be thousands depending on where you buy.

- Overstretching the monthly payment. A home you can’t comfortably carry makes every “savings” feel pointless.

Step-by-step roadmap for saving on your first home in 2026

1) Set your real budget first

- Choose a comfortable monthly payment range

- Add property taxes + condo fees (if applicable)

- Leave room for life (childcare, car, travel, emergencies)

2) Get pre-approved early

Pre-approval helps you:

- understand your price range

- catch credit/document issues early

- move faster when the right listing appears

[Internal link: pre-approval checklist]

3) Build your down payment stack

Common sources include:

- savings

- FHSA (if eligible)

- RRSP via HBP (if eligible)

- gifted down payment (documentation required)

4) Plan closing costs like a pro

Mini-checklist:

- legal fees + disbursements

- home inspection

- appraisal (if required)

- title insurance

- moving costs

- utility setup

5) Claim what you qualify for after closing

- home buyers’ amount (if eligible)

- provincial/municipal rebates (your lawyer/notary often helps with these)

- if applicable: GST/HST rebates for new housing (confirm eligibility carefully)

FAQ

Can I use the FHSA and the Home Buyers’ Plan together?

Often, yes—if you meet the conditions for each program at the time of the withdrawal(s) and the home qualifies.

How much can I contribute to an FHSA in 2026?

Annual participation room is generally $8,000 in the year you open your first FHSA, with a $40,000 lifetime limit.

What makes an FHSA withdrawal “qualifying”?

A qualifying withdrawal is tied to conditions including a first-time home buyer test and purchase/occupancy requirements.

What is the HBP limit in 2026?

The HBP withdrawal limit is $60,000 per eligible buyer.

What’s the home buyers’ amount and how much can I claim?

The home buyers’ amount is a non-refundable credit based on an amount you can claim (subject to eligibility and tax payable).

Do provinces offer rebates too?

Often, yes—but it depends where you buy. BC, Ontario, and Toronto are examples of jurisdictions with transfer-tax relief for eligible first-time purchasers.

A quick reminder before you make moves

Rules, limits, and eligibility can change—and your personal situation matters. This is general information, not tax, legal, or financial advice. Confirm details with official sources and qualified professionals before making decisions.

Soft next step

If you’d like, I can help you map out a 2026 purchase plan—how much you may need for down payment and closing costs, how to structure your FHSA/HBP approach, and what documents to have ready for a smooth approval.

Book a first-time buyer strategy call.