A vendor take back mortgage can help a real estate deal move forward when traditional financing does not fully cover the purchase. In simple terms, the seller agrees to finance part of the sale instead of receiving the full purchase price in cash at closing.

That flexibility can help bridge a financing gap, but it also changes the risk for everyone involved. The buyer takes on layered debt, the seller becomes a secured creditor, and any bank lender may still need to approve the structure.

This guide explains how a vendor take back mortgage works in Canada, when it may make sense, where it fits beside a bank mortgage, and what buyers and sellers should review before signing.

Need the practical version? Treat a VTB as a real mortgage, not a side agreement. If it is not documented, registered, and reviewed properly, the deal can become messy fast.

What Is a Vendor Take Back Mortgage?

A vendor take back mortgage, often shortened to VTB mortgage, is a form of seller financing. The seller lends part of the purchase price to the buyer and is repaid over time under agreed terms.

CMHC describes a vendor take-back mortgage as a situation where the person selling the home lends money to help make the sale.

In practice, that means the seller is not fully cashed out at closing. Instead, part of the sale price stays tied to the property as mortgage debt.

Because this is still mortgage financing, it should be documented like any other secured real estate loan.

A typical VTB agreement usually spells out:

- the amount being financed

- the interest rate

- payment frequency

- amortization

- term length or maturity date

- whether there is a balloon payment

- what happens on default

- where the VTB ranks against any first mortgage

Key takeaway: A vendor take back mortgage is seller financing secured by the property being sold.

How a Vendor Take Back Mortgage Usually Works in Canada

In many Canadian transactions, a VTB does not replace the bank mortgage. It sits beside it.

A common structure looks like this:

- the buyer brings some cash for the down payment and closing costs

- a bank or mortgage lender provides the first mortgage, if approved

- the seller finances an additional portion through a VTB

- both charges are documented and registered appropriately

Example scenario

A buyer agrees to purchase a property for $700,000.

- The buyer contributes cash at closing.

- The bank approves a first mortgage for part of the purchase.

- The seller leaves $50,000 to $100,000 in the deal as a vendor take back mortgage.

The buyer then repays the seller according to the agreement. That may involve monthly payments, interest-only payments, or a balloon payment at the end of the term.

CMHC underwriting materials specifically ask for details of any vendor take-back or second mortgage, including the amount, interest rate, amortization, and repayment terms. That is a strong reminder that this kind of financing must be clearly structured, not improvised at the last minute.

Is a Vendor Take Back Mortgage Legal in Canada?

Yes. A vendor take back mortgage is a legitimate financing arrangement in Canada when it is properly documented and registered.

What makes it serious is that mortgages are secured against real property. FCAC explains that a lender registers a charge against the property, which gives the lender legal rights if the borrower does not repay as agreed.

That same logic applies to a VTB. Even though the lender is the seller instead of a bank, the arrangement still affects title, enforcement rights, and discharge procedures.

Bottom line: A VTB is not a casual side promise. It is secured lending tied to the property and should be handled through lawyers.

Can a VTB Replace a Traditional Mortgage?

Sometimes, but not usually.

In most consumer transactions, a vendor take back mortgage works as a supplementary layer of financing rather than a full replacement for a bank mortgage.

Why? Because many buyers still need an institutional lender for the first mortgage, and that lender may still apply its normal underwriting rules.

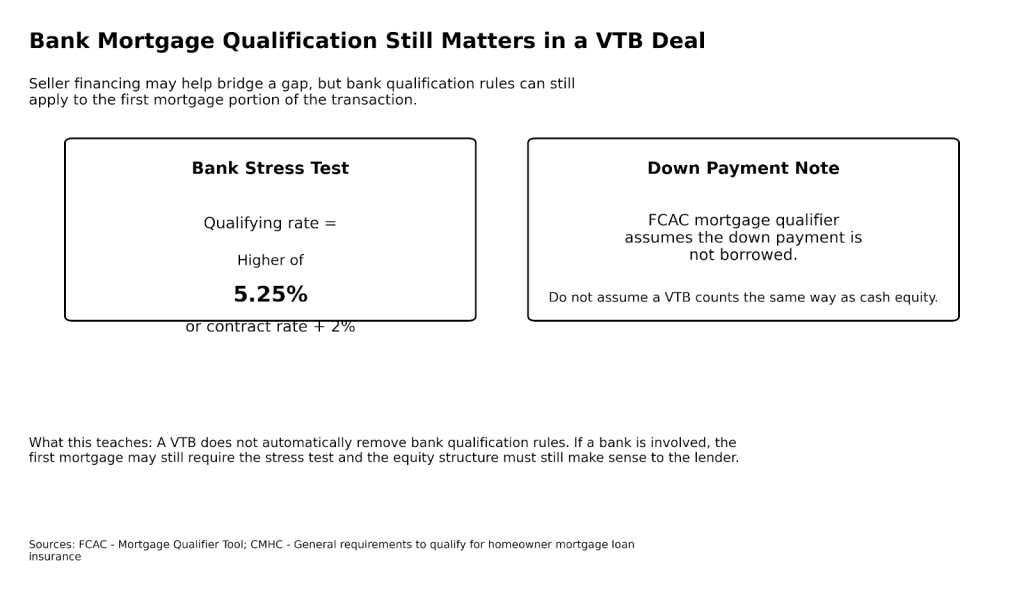

If a bank is involved, the mortgage stress test may still matter. FCAC says borrowers qualifying for a mortgage loan at a bank must pass the stress test using the higher of 5.25% or the contract rate plus 2%.

So while a VTB can help bridge a shortfall, it does not automatically remove the bank’s qualification standards.

VTB mortgage vs. bank mortgage

| Feature | Vendor Take Back Mortgage | Traditional Bank Mortgage |

| Who lends the money | Seller | Bank or lender |

| Security | Usually registered against the property | Registered against the property |

| Qualification style | Negotiated, plus any first-lender rules | Formal underwriting |

| Stress test | May still matter if a bank is involved | Applies at banks |

| Best fit | Financing gap or flexible sale structure | Standard home purchase |

Does a VTB Count as a Down Payment?

Not automatically.

This is one of the most misunderstood parts of VTB financing. Buyers sometimes assume seller financing can simply stand in for their required down payment, but that is not something to assume.

CMHC distinguishes between traditional and non-traditional down payment sources. It says traditional down payments can come from savings, sale proceeds from another property, or a non-repayable gift from a relative. It also says non-traditional sources must be arm’s length and not tied to the purchase and sale of the property, either directly or indirectly.

That matters because a VTB is tied directly to the transaction.

FCAC’s mortgage qualifier materials also assume the down payment is not borrowed. That does not answer every lender-specific scenario, but it is a clear warning sign: buyers should get lender confirmation early before relying on a VTB as part of the equity structure.

Practical takeaway: Do not assume a vendor take back mortgage will satisfy minimum down payment rules, especially in insured files.

Where the Main Risks Show Up

A vendor take back mortgage can solve one problem while creating several others.

Buyer risks

- taking on more total debt than the monthly budget can comfortably support

- agreeing to a short term with a balloon payout later

- assuming the deal works before the first lender fully approves the structure

- facing refinance pressure at maturity if the VTB must be paid out quickly

Seller risks

- not receiving the full sale proceeds at closing

- taking on repayment risk if the buyer defaults

- facing legal costs to enforce rights under the mortgage

- recovering less than expected if a first mortgage lender has priority

Because mortgage security is tied to title, these risks are not just financial. They can become legal and procedural very quickly.

What Should Be Included in a VTB Agreement?

A proper vendor take back mortgage agreement should be detailed enough that both sides understand the deal before closing.

At minimum, it should clearly address:

- how much the seller is financing

- the interest rate

- the payment amount and payment schedule

- amortization period

- maturity date

- whether there is a balloon payment

- priority ranking behind any first mortgage

- default provisions and enforcement rights

- discharge terms once the debt is repaid

FCAC explains that mortgage discharge and title changes usually involve the provincial or territorial land title registry process, often with help from a lawyer or notary.

That is why a VTB should be treated as lawyer territory from the beginning.

Are There Tax Consequences for the Seller?

Potentially, yes.

When a seller gets paid over time instead of receiving the full proceeds at closing, tax timing may become part of the planning process.

CRA says that when a seller claims a capital gains reserve, the gain is still calculated for the year of disposition, but some of the gain may be deferred under the reserve rules. CRA also says that, generally, most reserves can be claimed over a maximum period of 4 years, which results in the total capital gain being included in income over 5 years.

That does not mean every seller should use a reserve or will qualify in the same way. It means a VTB can create tax planning questions that should be discussed before closing, not after.

If you are the seller, get tax advice before agreeing to long payout terms.

Step-by-Step Roadmap for Using a Vendor Take Back Mortgage

The safest VTB process starts before the offer is locked in.

- Measure the financing gap. Know exactly how much money is missing and whether a VTB is truly needed.

- Check first-lender rules early. If a bank is involved, ask whether the lender will permit the VTB and on what terms.

- Model the full payment load. Include the bank mortgage, VTB payment, taxes, heating, and any condo fees.

- Set the legal terms clearly. Amount, rate, amortization, maturity, priority, and default language should all be written down.

- Use lawyers for both sides. This is secured real estate lending, not an informal family arrangement.

- Review tax timing. Sellers paid over time should talk to a tax advisor about capital gains reserve rules and reporting.

- Plan the exit. Decide whether the VTB will be repaid by refinance, sale, or scheduled repayment.

Why Professional Help Matters

A vendor take back mortgage is one of those deals that can look simple in conversation and become complicated on paper.

That is why professional review matters on both the mortgage side and the legal side.

A mortgage professional can help assess:

- whether the first lender will accept the structure

- whether the total payment load is realistic

- whether the buyer still qualifies under bank rules

- whether another financing strategy may be cleaner

A real estate lawyer can help ensure:

- the charge is documented properly

- registration and priority are handled correctly

- default language is enforceable

- discharge terms are clear when the debt is repaid

Example scenario

A buyer and seller agree verbally that the seller will leave money in the deal to help close. Everyone feels comfortable because the numbers seem close enough to work.

Then the first lender asks for full VTB details, the lawyers discover gaps in the repayment terms, and the closing timeline gets tight.

That kind of stress is exactly why the VTB structure should be reviewed early, not after the offer is already moving toward closing.

FAQs

Is a vendor take back mortgage legal in Canada?

Yes. It is a legitimate form of seller financing when it is properly documented and registered.

Is a VTB mortgage usually a second mortgage?

Often, yes, but not always. In many transactions it sits behind a first mortgage, although the exact ranking depends on the deal.

Can a VTB help me avoid the mortgage stress test?

Not on the bank portion of the financing. If a bank mortgage is involved, the bank’s qualification rules may still apply.

Can I use a VTB as my down payment?

Do not assume that. Buyers should confirm with the lender and insurer, because seller financing tied to the deal may not be treated the same way as cash equity.

What happens if the buyer stops paying?

Because the VTB is secured against the property, the seller may have legal rights tied to enforcement. The practical outcome depends on the mortgage terms, provincial procedures, and priority ranking.

Are there tax issues when the seller gets paid over time?

Potentially, yes. A seller may need tax advice on capital gains timing and reserve rules before agreeing to installment-style proceeds.

Should both parties use separate lawyers?

Yes. Separate legal advice is usually the safer approach because the transaction affects title, security, repayment rights, and discharge procedures.

Final Takeaways

If you are considering a vendor take back mortgage in Canada, keep these three points in mind:

- A VTB is real mortgage financing, not an informal side deal.

- It often works best as a gap-filling layer beside a first mortgage, not as a simple replacement for normal underwriting.

- The biggest mistakes usually come from weak documentation, unclear repayment terms, or assumptions about down payment and lender approval.

Before you sign, get the full structure reviewed. A mortgage professional can assess whether the deal works from a lending standpoint, and a real estate lawyer can make sure title, priority, and repayment rights are set up properly.

That extra work upfront may help you avoid closing delays, enforcement problems, and expensive misunderstandings later.

Disclaimer: This article is general information, not legal, tax, or mortgage advice. A vendor take back mortgage may affect title, repayment rights, tax reporting, and lender approval, so buyers and sellers should get legal and mortgage advice before signing.

Sources & References

Canada Mortgage and Housing Corporation, Starting Your Search for a Home

https://www.cmhc-schl.gc.ca/professionals/industry-innovation-and-leadership/industry-expertise/resources-for-mortgage-professionals/starting-your-search-for-home

Financial Consumer Agency of Canada, Mortgage Qualifier Tool

https://itools-ioutils.fcac-acfc.gc.ca/MQ-HQ/MQ-EAPH-eng.aspx

Financial Consumer Agency of Canada, Mortgage security: know your rights

https://www.canada.ca/en/financial-consumer-agency/services/rights-responsibilities/rights-mortgages/rights-mortgage-security.html

Financial Consumer Agency of Canada, Discharging a mortgage

https://www.canada.ca/en/financial-consumer-agency/services/mortgages/mortgage-discharge.html

Canada Mortgage and Housing Corporation, General requirements to qualify for homeowner mortgage loan insurance

https://www.cmhc-schl.gc.ca/consumers/home-buying/mortgage-loan-insurance-for-consumers/what-are-the-general-requirements-to-qualify-for-homeowner-mortgage-loan-insurance

Canada Mortgage and Housing Corporation, Required Documentation Guide

https://assets.cmhc-schl.gc.ca/sf/project/cmhc/pdfs/content/en/required-documentation.pdf

Canada Mortgage and Housing Corporation, Replacement of Covenant

https://assets.cmhc-schl.gc.ca/sf/project/cmhc/pdfs/content/en/replacement-of-covenant.pdf

Canada Revenue Agency, Claiming a capital gains reserve

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/about-your-tax-return/tax-return/completing-a-tax-return/personal-income/line-12700-capital-gains/claiming-a-capital-gains-reserve.html

Financial Consumer Agency of Canada, Mortgage prepayment: know your rights

https://www.canada.ca/en/financial-consumer-agency/services/rights-responsibilities/rights-mortgages/rights-prepayments.html