If you are shopping for a home in Canada right now, mortgage rate strategy is about more than guessing whether rates will rise or fall.

The real question is whether you can lock a useful rate for a long enough window, on the right mortgage product, without paying extra for certainty you do not actually need. The Financial Consumer Agency of Canada says a pre-approval may let you lock in an interest rate for 60 to 130 days, depending on the lender. That makes timing important right away.

In 2026, mortgage rate decisions also sit inside a wider policy and qualification backdrop. The Bank of Canada maintained its policy rate at 2.25% on March 18, 2026, and its next scheduled rate announcement is April 29, 2026. But locking now is not just a Bank of Canada call. Fixed and variable mortgages behave differently, lender hold policies differ, and the stress test can still affect what you qualify for even after you lock.

This guide explains how a mortgage rate lock works in Canada, when it helps, when it can backfire, and how to choose a 2026 strategy that protects your budget without leaving you overpaying.

Want a quick sanity check before you decide? See our mortgage pre-approval guide, fixed vs. variable mortgage guide, and mortgage closing costs checklist.

Quick Answer

In Canada, locking a mortgage rate usually means getting a pre-approval or lender rate hold that protects pricing for a limited period while you shop or move toward closing. The FCAC says those holds may last 60 to 130 days depending on the lender, and large lenders such as RBC,TD, and CIBC currently advertise 120-day pre-approval holds.

Locking can make sense if you are buying soon, want payment certainty, or need to protect qualification against rising rates. It can cost you money if you lock too early, lock the wrong product, or compare only the headline rate instead of penalties, flexibility, and stress-test impact.

Key takeaway: The best mortgage rate lock is the one that matches your real buying timeline, not the one that simply sounds safest.

What does it mean to lock a mortgage rate in Canada?

A rate lock is a lender commitment, usually tied to a pre-approval or approval, that holds a specific rate or pricing for a limited period while you look for a property or move toward closing.

It is not the same as unconditional final approval.

The FCAC’s pre-approval guidance says the process may let you:

- know the maximum mortgage amount you could qualify for

- estimate your mortgage payments

- lock in an interest rate for 60 to 130 days, depending on the lender

In practice, many major lenders advertise a 120-day version of that promise. RBC says its mortgage pre-approval includes a 120-day rate guarantee. TD says a pre-approval offers a rate hold of up to 120 days, subject to conditions. CIBC says its pre-approval certificate guarantees the interest rate for up to 120 days, provided your financial situation does not change.

That last condition matters. A rate lock does not mean every part of your file is settled. Property details, appraisal, income, debts, credit, and final underwriting can still change the outcome.

A simple definition to remember: a mortgage rate lock is a temporary pricing shield, not a full promise that your mortgage will fund on those exact terms no matter what changes later.

When should you lock a mortgage rate?

Locking usually makes the most sense when your purchase timeline fits comfortably inside the lender’s hold window and payment certainty matters more to you than the chance of a slightly lower rate later.

Right now, the backdrop is still uncertain. In its March 18, 2026 opening statement, the Bank of Canada said uncertainty related to U.S. trade policy and broader geopolitical risks remains elevated. That does not tell you exactly where mortgage pricing will go next month, but it does mean the environment is not calm enough to assume rates will neatly drift in your favour.

A lock is usually strongest when:

- you expect to buy or close within the next 30 to 120 days

- your budget is tight enough that even a modest rate increase would matter

- you are near the edge on qualification and want to protect borrowing power

- you already know whether fixed or variable fits your situation better

A lock is usually weaker when:

- you are still six months or more away from buying

- your product choice is still unsettled

- you are trying to call the exact market bottom

- your hold window may expire before closing

There is one useful detail buyers often miss. TD says that once you are pre-approved, it will hold your rate for 120 days subject to conditions, and its pre-approval materials also say you can ask to have the rate adjusted if the applicable rate drops during the hold period. That means some rate holds allow downward repricing, but not all lenders treat this the same way.

Decision checkpoint: If your closing date is likely to land outside the hold period, a rate lock may feel reassuring without giving you real protection.

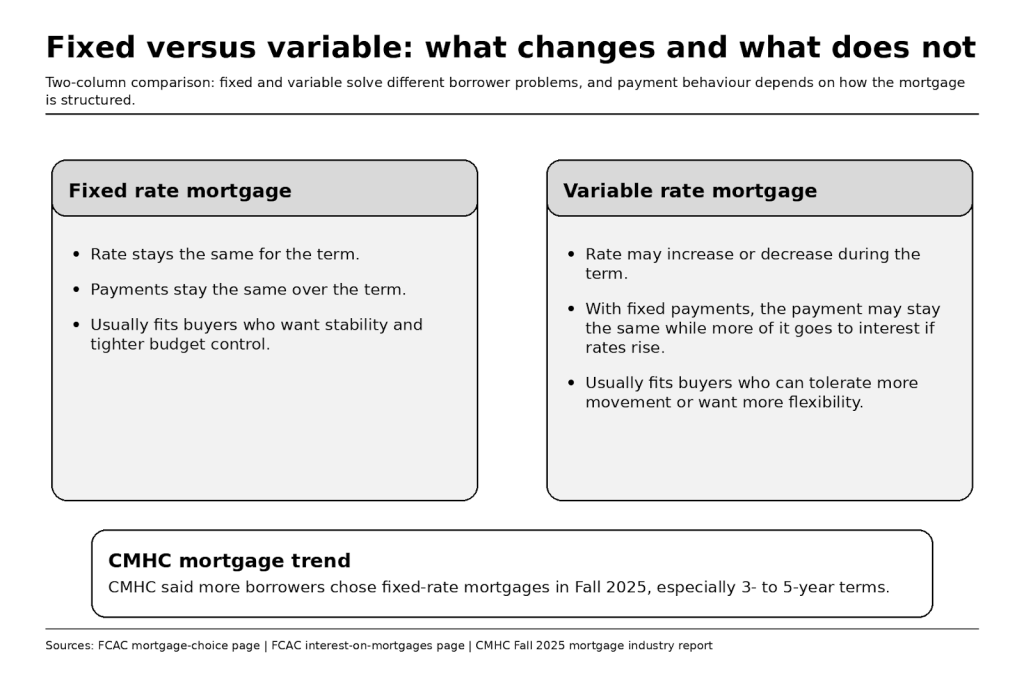

Is fixed or variable the better 2026 strategy?

Neither is automatically better. The right answer depends on your risk tolerance, your timeline, and how much certainty your budget needs.

The FCAC says a fixed-rate mortgage may suit borrowers who want to keep payments the same during the term, know in advance how much principal they will pay down, or keep their rate steady because they think market rates may rise. It also says a variable-rate mortgage with fixed payments may be riskier than buyers expect because, when rates rise, more of each payment goes toward interest costs.

The FCAC’s broader mortgage-choice guide also notes that a variable rate is typically lower than a fixed rate for a similar term, but that lower starting point comes with more movement risk.

CMHC’s Fall 2025 Residential Mortgage Industry Report page and its related In-House podcast summary say more borrowers have been choosing fixed-rate mortgages, especially 3- to 5-year terms. That does not prove fixed is best for every household, but it does show how many borrowers reacted after years of rate volatility.

Here is the practical comparison:

| Feature | Fixed rate | Variable rate |

| Payment stability | Usually steadier over the term | May change, or may become riskier if payments stay fixed while rates rise |

| Starting price | Often higher than a comparable variable rate | Often lower than a comparable fixed rate |

| Best for | Buyers who value predictability and budget control | Buyers who can tolerate movement and want more pricing flexibility |

| Main risk | Paying more than necessary if rates fall after you lock | Payment shock, slower principal paydown, or trigger-rate issues if rates rise |

The better question is not “Which wins in theory?” It is “Which one lets me qualify, close, and still sleep at night?”

Why can a rate lock still leave you overpaying?

Buyers often overpay by locking the wrong mortgage, not just the wrong rate.

A low advertised number can distract from the rest of the contract. The FCAC says you should compare more than interest rate alone, including:

- term

- amortization period

- payment frequency

- fixed versus variable structure

- prepayment privileges

Those details affect your total cost just as much as the headline percentage.

Overpaying also happens when buyers lock before they have a realistic closing timeline. If your purchase drifts beyond the hold period, you may need to restart at a new market price anyway.

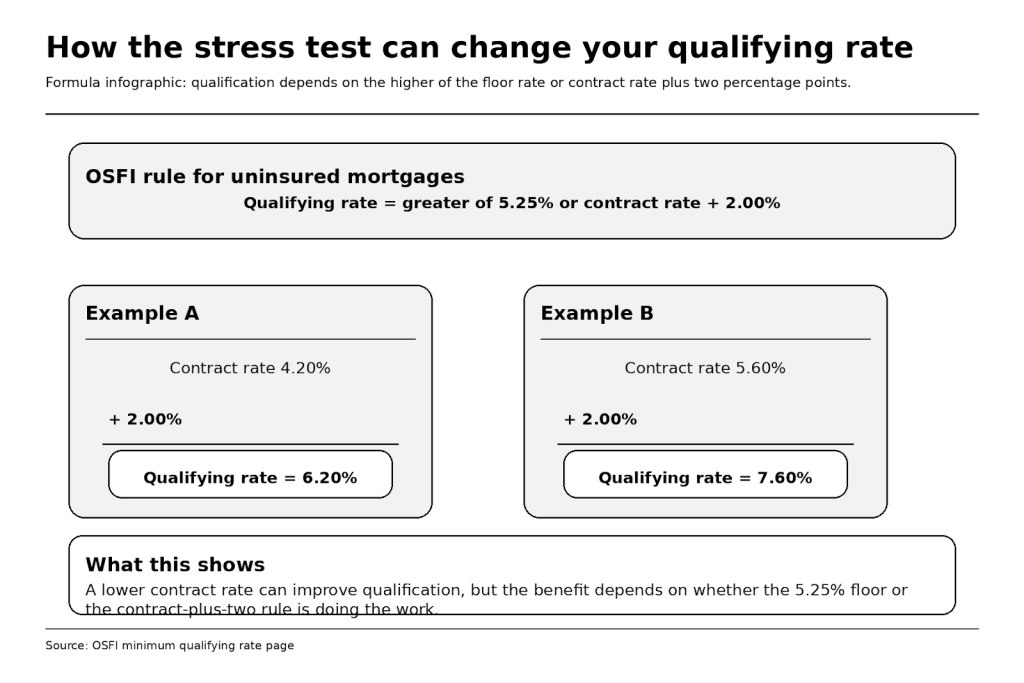

There is also a qualification angle. If you choose a higher contract rate than necessary, you may increase your stress-test qualifying rate too. The OSFI says the minimum qualifying rate for uninsured mortgages at federally regulated lenders remains the greater of 5.25% or the contract rate plus 2 percentage points.

Bottom line: A mortgage rate lock can protect you from a rate increase, but it can also quietly raise your total cost if you choose the wrong structure or timing.

How does the stress test affect your rate-lock strategy?

The stress test can make rate strategy more important because qualification depends on more than your actual payment.

For uninsured mortgages at federally regulated lenders, the OSFI’s minimum qualifying rate rule remains the greater of 5.25% or contract rate plus 2%.

That means a lower contract rate can sometimes help qualification, but not always.

- If your contract rate is low enough that 5.25% is still the higher number, getting a slightly better rate may not change the qualifying rate at all.

- If your contract rate is high enough that contract rate + 2% is above 5.25%, the rate you lock can directly affect qualification.

The FCAC’s mortgage-preparation page specifically tells buyers to understand how the stress test affects qualification before they shop.

That is why locking is not only a pricing decision. It is also a financing-risk decision. If you are close to the edge on debt-service ratios, protecting qualification may matter more than chasing the last possible discount.

What is the practical way to lock without overpaying?

Start with your timeline, then your qualification, then your product choice. Lock only after those pieces are clear.

A practical roadmap looks like this:

- Set your real timeline. Are you buying in 30 days, 90 days, or “sometime this year”? The FCAC’s 60-to-130-day range makes this your first filter.

- Check qualifications first. If your debt ratios are tight, the stress test may matter more than a small headline discount.

- Choose your product family before locking. Fixed and variable solve different problems.

- Ask how repricing works if rates fall. Some lenders will revisit the rate during the hold period, but not all.

- Compare penalties and prepayment options. A slightly lower rate can still be more expensive overall if the contract is costly to break or too restrictive.

- Refresh your file before closing. CIBC says changes to your financial situation between pre-approval and final approval can affect the amount you qualify for.

What common mistakes do buyers make?

Most mistakes happen when buyers treat the rate hold as the entire mortgage strategy.

Common examples include:

- locking before you know your real timeline

- comparing only rate instead of contract features

- ignoring stress-test math

- assuming a pre-approval is the same as final approval

- choosing variable without understanding payment mechanics

- failing to ask whether the hold can improve if rates fall

- waiting too long before renewal or early-renewal review

TD says on its mortgage pre-approval and mortgage pages that pre-approval offers up to a 120-day hold, and its mortgage materials also point to early timing options in the mortgage journey. That makes timing strategy relevant for renewers too, not only first-time buyers.

Frequently asked questions

How long does a mortgage rate hold last in Canada?

The FCAC says lenders may lock in a rate for 60 to 130 days, depending on the lender. RBC,TD, and CIBC all currently advertise 120-day pre-approval holds.

Does a pre-approval guarantee my final mortgage rate?

Not automatically. A pre-approval can include a rate hold, but final approval still depends on conditions such as the property, valuation, credit, and your financial profile at closing.

Is fixed or variable better in Canada in 2026?

It depends on your risk tolerance and budget. The FCAC says fixed rates offer more payment certainty, while variable products can move and may create more risk in some payment structures.

Can I get a lower rate if rates fall after I lock?

Sometimes. Some lenders allow downward repricing during the hold period, subject to conditions. Buyers should ask this directly because rate-hold policies are not identical across lenders.

Does the mortgage stress test still matter if I lock a rate?

Yes. The OSFI says the minimum qualifying rate for uninsured mortgages remains the greater of 5.25% or contract rate plus 2%.

When should I lock a mortgage rate before closing?

Usually when your closing is close enough to fit inside the hold period and you would be meaningfully affected by a rate increase. If you are still far from buying, locking may be more psychological than practical.

Why professional help still matters

A lender pre-approval gives you a number. It does not always tell you whether you picked the right strategy.

A mortgage professional can help with the parts generic rate-shopping does not solve well, including:

- whether fixed or variable fits your actual risk tolerance

- whether a lower rate is worth a worse penalty structure

- whether your hold period realistically covers your closing date

- whether your qualification risk matters more than your pricing risk

That kind of review matters because the wrong mortgage rate strategy usually costs money in ways buyers do not notice until later.

What should you remember before you lock?

Before you lock, keep these three points in mind:

- A mortgage rate lock is a tool, not a prediction.

- The best lock is the one that protects your real timeline and qualification risk.

- A slightly lower advertised rate is not automatically the cheaper mortgage.

Stop guessing. Before you commit, ask for the hold period, repricing policy, penalty structure, prepayment rights, and stress-test impact in writing. That is the fastest way to see whether the rate you are locking is actually helping you.

If you want help comparing a 120-day hold, a fixed option, and a variable option for your own purchase, speak with a Pegasus mortgage professional for a side-by-side review.

Disclaimer: This article is general information, not personal mortgage advice. Rate holds, pre-approvals, final approvals, and available pricing vary by lender, property, down payment, credit profile, and whether the mortgage is insured or uninsured. Mortgage pricing can change quickly, so confirm current options before you sign anything. FCAC says pre-approvals may let you lock in a rate for 60 to 130 days depending on the lender.

Sources & References

- Financial Consumer Agency of Canada — Getting preapproved for a mortgage

https://www.canada.ca/en/financial-consumer-agency/services/mortgages/preapproval-qualify-mortgage.html - Financial Consumer Agency of Canada — Choosing a mortgage that is right for you

https://www.canada.ca/en/financial-consumer-agency/services/mortgages/choose-mortgage.html - Financial Consumer Agency of Canada — Interest on mortgages

https://www.canada.ca/en/financial-consumer-agency/services/mortgages/interest-on-mortgages.html - Financial Consumer Agency of Canada — Preparing to get a mortgage

https://www.canada.ca/en/financial-consumer-agency/services/mortgages/preparing-mortgage.html - Bank of Canada — Monetary Policy Decision Press Conference Opening Statement (March 18, 2026)

https://www.bankofcanada.ca/2026/03/opening-statement-2026-03-18/ - Bank of Canada — Upcoming events / scheduled interest rate announcements

https://www.bankofcanada.ca/press/upcoming-events/ - Office of the Superintendent of Financial Institutions — Minimum qualifying rate for uninsured mortgages

https://www.osfi-bsif.gc.ca/en/supervision/financial-institutions/banks/minimum-qualifying-rate-uninsured-mortgages - RBC Royal Bank — Mortgage Pre-Approval

https://www.rbcroyalbank.com/mortgages/getting-preapproved.html - TD Canada Trust — Mortgage Pre-Approval

https://www.td.com/ca/en/personal-banking/products/mortgages/first-time-home-buyer/pre-approval - TD Canada Trust — Fixed Rate Mortgages

https://www.td.com/ca/en/personal-banking/products/mortgages/fixed-rate-mortgages - CIBC — Get a Mortgage Pre-Approval Certificate

https://www.cibc.com/en/personal-banking/mortgages/resource-centre/preapproval.html - CMHC — Residential Mortgage Industry Report

https://www.cmhc-schl.gc.ca/professionals/housing-markets-data-and-research/housing-research/research-reports/housing-finance/residential-mortgage-industry-report - CMHC — In-House Podcast: Fall 2025 Residential Mortgage Industry Report insights

https://www.cmhc-schl.gc.ca/observer/2025/in-house-podcast-fall-residential-mortgage-industry-report-insights