When deciding between a 25 or 30-year mortgage amortization period, the key difference lies in the length of time it takes to repay your loan. A 30-year amortization typically results in lower monthly payments but higher interest costs over the life of the loan, while a 25-year period may offer quicker equity buildup and lower overall interest costs. The best choice depends on your financial goals, current budget, and long-term plans.

When you’re taking out a mortgage, one of the most important decisions you’ll face is how long it will take to pay off the loan. The most common options for amortization in Canada are 25-year and 30-year periods, but how do you know which is best for your situation? While both options have their benefits, the decision can significantly impact your monthly payments and the total interest paid over the life of the mortgage. In this article, we’ll break down what each option means for you and help you make an informed choice. Whether you’re looking for lower monthly payments or faster repayment, understanding these choices is the first step in finding the best mortgage plan for your future.

Quick Start: Pick Your Path

Choose the section that best matches your situation:

- Looking for lower monthly payments? → Read about the 30-year mortgage.

- Want to pay off your mortgage sooner and save on interest? → Check out the 25-year mortgage option.

- Unsure which option is better for your budget? → Learn how to make an informed decision.

What Is Mortgage Amortization?

Mortgage amortization is the process of gradually paying off your mortgage loan through fixed payments over a set period of time. It’s important because it determines how long it will take to fully repay your loan, and how much of your monthly payment goes toward the loan principal versus interest.

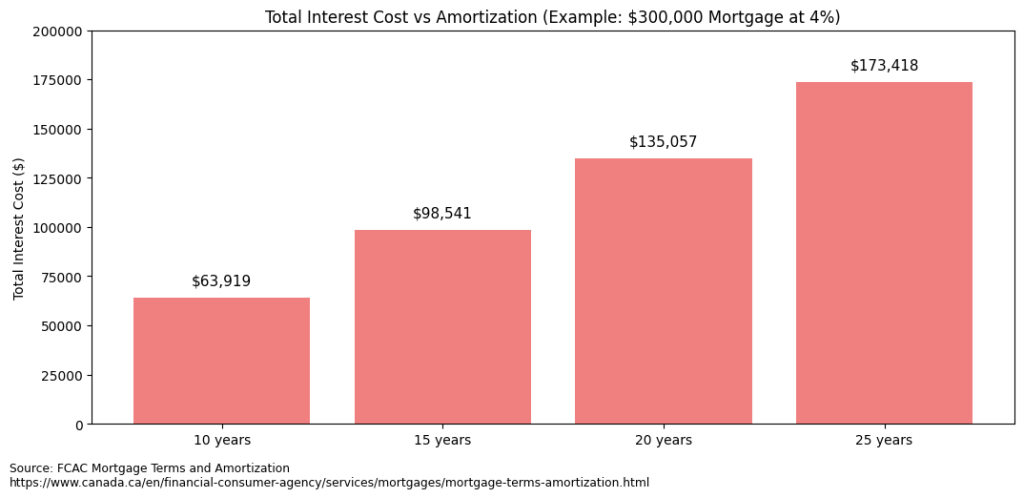

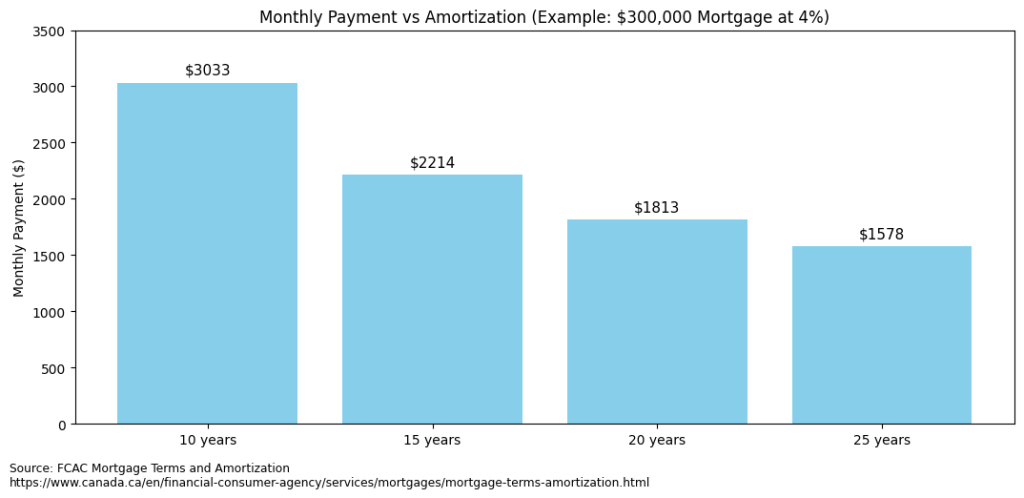

Mortgage amortization periods in Canada typically range from 15 to 30 years, with 25 and 30 years being the most common choices for homeowners. The longer the amortization period, the lower your monthly payments, but you may end up paying more interest in the long run. A shorter amortization period results in higher payments but less interest paid over the life of the loan.

25 vs. 30-Year Mortgage Amortization: What’s the Difference?

Which is better: 25 or 30-year mortgage amortization?

The key difference between a 25-year and a 30-year mortgage is the length of time it takes to pay off your loan. A 30-year period gives you lower monthly payments, but it results in higher total interest payments over time. A 25-year mortgage reduces your total interest costs but results in higher monthly payments.

Choosing between these two options depends on your budget, goals, and ability to handle higher monthly payments.

Monthly Payment Differences: 25-Year vs. 30-Year Amortization

The most obvious difference between a 25 and 30-year mortgage is how much you’ll pay each month. A 30-year amortization will give you lower monthly payments, making it more affordable in the short term. However, over the life of the loan, you will pay more interest. Here’s a breakdown:

| Feature | 25-Year Amortization | 30-Year Amortization |

| Monthly Payment | Higher | Lower |

| Total Interest Paid | Lower | Higher |

| Time to Repay Mortgage | Shorter | Longer |

| Ideal for | Higher income earners | Budget-conscious buyers |

The lower payments of a 30-year mortgage are appealing for those who need the extra room in their budget, but over the years, the extra interest could add up to a significant amount.

How Does Amortization Affect Your Mortgage?

Why does amortization impact your mortgage payment?

The longer the amortization period, the smaller your monthly payment, but the more you will pay in total interest. A shorter period means larger monthly payments but less interest paid in total.

This is because interest is calculated on the outstanding balance of the loan. With a 30-year amortization, you pay less of the principal early on, so the interest payments remain higher for a longer period. In contrast, with a 25-year mortgage, the principal is paid off more quickly, which reduces the interest over time.

Deciding Between 25-Year and 30-Year Amortization

How do I decide between a 25-year and 30-year mortgage?

Your decision should be based on your budget and long-term financial goals. If you can afford higher payments and want to pay off your mortgage faster, a 25-year amortization is a good choice. If lower monthly payments are more important to you, a 30-year mortgage could be a better option.

It’s essential to consider how your monthly payment fits into your overall budget and whether you’ll be comfortable with higher payments over a shorter time.

Mortgage Amortization: Impact on Equity and Interest

While the main differences between a 25-year and 30-year mortgage lie in payment size and interest, another important factor is the rate at which you build equity in your home. With a 25-year mortgage, you pay off more principal each month, which means you build equity faster. With a 30-year mortgage, the rate at which you build equity is slower because you’re paying off less of the principal in the earlier years of the loan.

Common Mistakes to Avoid When Choosing Amortization

- Choosing based solely on monthly payment:

While the lower payment of a 30-year mortgage may seem appealing, consider the total cost of the loan over its lifetime. - Underestimating future budget changes:

Don’t assume your budget will stay the same for 30 years. Life changes could affect your ability to pay off a 30-year mortgage. - Ignoring interest savings over the loan term:

A 25-year mortgage can save you a substantial amount of money in interest, even if the monthly payment is higher. - Not considering your ability to refinance or pay extra:

If you plan to refinance in the future, a shorter amortization may allow for more flexibility. - Assuming the lowest payment is always the best option:

Weigh the long-term costs, not just the short-term savings.

FAQ Section

What is the standard mortgage amortization period in Canada?

In Canada, the standard mortgage amortization period is typically 25 years, although 30-year options are also common. Canada Mortgage and Housing Corporation (CMHC) guidelines often encourage 25 years as the ideal period, but 30 years are available for some buyers who meet specific eligibility criteria.

Is a 30-year mortgage worth it?

A 30-year mortgage can be a good choice for buyers seeking lower monthly payments. However, it results in paying more interest over time. It’s ideal for those who need more room in their budget but can still afford the overall loan payments.

Can I pay off my mortgage early with a 30-year amortization?

Yes, you can pay off your mortgage early, but doing so depends on your lender’s terms and whether they allow prepayments without penalty. Paying extra towards your principal can significantly reduce the interest you pay.

Will my mortgage rate change with a longer amortization?

Mortgage rates typically don’t change based on the length of amortization but can vary depending on your creditworthiness, lender, and current market conditions. Make sure to check with your lender about the best rates available for your mortgage term and amortization.

How much extra will I pay on a 30-year mortgage compared to 25 years?

You will pay more in total interest over the life of a 30-year mortgage compared to a 25-year mortgage. While monthly payments are lower, the overall cost of the loan increases.

Should I choose a shorter amortization if I can afford higher payments?

If you can afford the higher payments, a shorter amortization may be a good option since it allows you to pay off your mortgage faster and reduce the interest you pay. It’s ideal if you plan to stay in the home long-term and want to build equity more quickly.

Closing Section

Choosing between a 25 or 30-year mortgage is a crucial decision that affects both your monthly budget and the total amount you’ll pay for your home. It’s important to consider your current financial situation, long-term goals, and the overall costs before making your decision. For personalized advice, reach out to a mortgage professional who can guide you through the best option based on your unique circumstances.

Sources & References

- Canada Mortgage and Housing Corporation (CMHC)

https://www.cmhc-schl.gc.ca - Bank of Canada Mortgage Rates

https://www.bankofcanada.ca - Government of Canada – Mortgage Rules and Policies

https://www.canada.ca/en/services/mortgages