If you’ve been watching Canada home prices in 2026, it probably feels like the market is talking out of both sides of its mouth. One headline says prices are down. Another says a city is booming. Your friend in Winnipeg is still seeing competition, while your cousin in Ontario says showings are quieter.

And then there’s the mortgage payment—where even a “softer” price can still feel expensive.

You’re not imagining it. In the housing market 2026 Canada, there are “hidden gaps”: differences between regions, property types, and even how prices are measured. Those gaps can change what you can afford, how you negotiate, and which mortgage strategy fits your real life.

Quick start: Pick your path

Choose the closest match and focus on the sections that matter most.

If you’re buying your first home

- Learn the difference between average prices and the MLS Home Price Index Canada

- Watch your payment budget, not just the listing price

- Compare neighbourhood-level trends, not national headlines

If you’re moving up or downsizing

- Track the gap between the home you’re selling and the one you’re buying

- Pay attention to property-type splits (condo vs. detached)

- Plan for closing-date timing and rate holds

If you’re relocating between provinces

- Expect a regional housing market split

- Use city-level data (not provincial averages) to set expectations

- Build a “new market” pre-approval plan before you house-hunt

If you’re renewing your mortgage

- Focus on affordability and payment planning first

- Review options like refinance, switch, or blend-and-extend (where available)

- Stress-test your budget for life changes

What “hidden gaps” actually mean

Hidden gaps are the reasons two people can read the same “Canada home prices” headline and have totally different experiences.

Common gaps include:

- Regional gaps: one province or city rises while another declines

- Property-type gaps: condos and detached homes move differently

- Measurement gaps: indexes vs. averages can tell different stories

- Timing gaps: one area turns months before another

- Affordability gaps: small price changes can feel huge when payments change

A solid 2026 plan is less about predicting one national number—and more about understanding which gap affects your purchase.

Key takeaway: The headline isn’t the market. Your city + your property type + your payment determines your reality.

The 2026 backdrop: why the market feels uneven

1) Interest rates set the mood, but not every city reacts the same

In late January 2026, the Bank of Canada held its policy rate at 2.25%. That matters because the policy rate influences borrowing costs across the economy, including variable-rate mortgage pricing (and indirectly, many fixed-rate dynamics).

What that means in plain English:

- In high-price markets, even a small change in borrowing costs can push a lot of buyers out of qualifying.

- In more affordable markets, demand can hold up better—so prices can look steadier.

2) Demand is softer nationally, but not evenly

Nationally, Canadian home sales fell 5.8% month-over-month in January 2026. But the slowdown wasn’t evenly distributed—parts of Ontario saw a bigger drop in activity than many other regions.

Translation: a national number can be technically accurate and still not match what’s happening on your block.

3) Supply and construction patterns differ by region

CMHC’s 2026 outlook highlights a clear split:

- Ontario and British Columbia: expected to be weaker than their 10-year averages

- Prairies and Quebec: expected to remain above historical averages

- Ontario: flagged as the only region expected to see price declines in 2026

That’s one reason you can see an Ontario slowdown alongside Prairie resilience and Quebec strength at the same time.

Decision checkpoint: If you’re buying in a softer market, negotiation room may be better—but your payment still has to work.

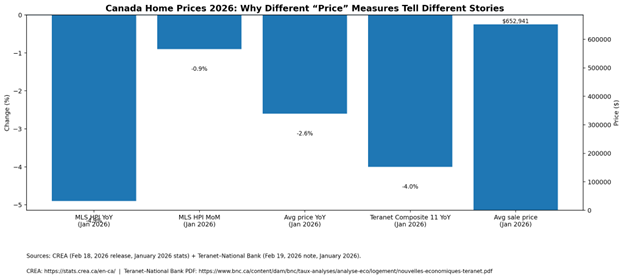

The gap most people miss: not all “price” measures mean the same thing

Many people compare:

- the average sale price

- the MLS Home Price Index (HPI)

- repeat-sales indexes (like Teranet–National Bank)

…but these can move differently because they measure different things.

Average sale price: sensitive to the “mix” of homes sold

Average sale price can swing based on what sold that month.

Example: if fewer luxury detached homes sell and more condos sell, the average can fall—even if the “typical” home didn’t change much.

MLS® HPI: designed to track a “typical” home over time

The MLS Home Price Index Canada aims to reduce the mix problem by comparing like-with-like over time.

That’s why you can see:

- a modest change in average price, but

- a larger (or smaller) shift in HPI—

…and both can be true.

Repeat-sales indexes: track the same homes across multiple sales

Repeat-sales indexes (like Teranet–National Bank) focus on properties that sell more than once. It’s another way to track price change without the “mix” distortions of average price.

So here’s the move: Use the most local, most comparable measure you can find—city/neighbourhood + property type beats national headlines.

The regional housing market split: why Canada doesn’t move as one market

This is where the “hidden gaps” become very real.

Ontario: affordability pressure shows up first

When rates and payments pinch, higher-priced markets often feel it first.

That can look like:

- longer days on market in certain suburbs

- more price reductions

- more conditional offers (financing, inspection)

It can also show up unevenly—some neighbourhoods cool before others.

Prairies: resilience can be an affordability story

More affordable markets can hold up better because a larger share of buyers can still qualify and carry the payment.

Quebec: strong city-level gains can coexist with soft national headlines

Quebec’s big cities can show strength even when the national picture looks flat-to-down.

Net-net: Canada home prices in 2026 are not one story—they’re a cluster of local stories.

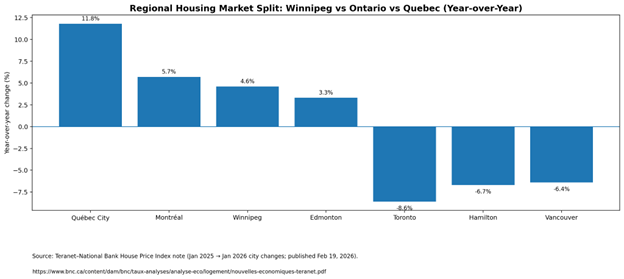

City-level reality: Winnipeg vs. parts of Ontario (and why it matters)

When someone says “the market,” ask: which market?

From the Teranet–National Bank repeat-sales data (Jan 2025 → Jan 2026), the gap is obvious:

- Winnipeg: +4.6% year-over-year

- Toronto: -8.6% year-over-year

- Hamilton: -6.7% year-over-year

- Vancouver: -6.4% year-over-year

- Montréal: +5.7% year-over-year

- Québec City: +11.8% year-over-year

That’s the “hidden gap” in one glance: affordability, supply, and local economies don’t line up the same way across Canada.

Another gap: condo vs. detached (and new builds vs. resale)

Even within the same city, pricing can split based on what people are buying.

Condo and detached markets can behave differently because they attract different buyers:

- condos often skew toward first-time buyers and investors

- detached homes skew toward move-up buyers and families

Supply also matters. CMHC has noted condominium construction can be especially weak in some markets, while purpose-built rental has been a major driver of new supply.

What this means for you:

- If you’re buying a condo, your negotiation leverage and appraisal risk can look different from a detached buyer two streets away.

- Your mortgage strategy (down payment, rate hold, closing flexibility) should match the segment you’re in.

Decision checkpoint: If your target segment has lots of competing listings, you can often negotiate terms—not just price.

Common mistakes buyers make in 2026

- Using national headlines to decide on a local purchase (your neighbourhood can diverge)

- Confusing average price with typical value (average price is sensitive to the mix of sales)

- Shopping homes before confirming payment comfort (qualifying and budgeting are different)

- Ignoring property-type splits (condo vs. detached can behave differently)

- Assuming “prices down” automatically means “easy to buy” (payments and qualifying still matter)

- Waiting until the offer stage to think about financing conditions (you want a plan before you negotiate)

Key takeaway: The buyer who wins in 2026 isn’t the one who “predicts prices”—it’s the one who is prepared and payment-clear.

A step-by-step roadmap to navigate Canada home prices in 2026

1) Start with your payment number

Before you fall in love with a listing, set a payment range you can actually live with.

- Decide your monthly comfort range (not your maximum approval)

- Leave room for utilities, maintenance, and life surprises

- If renewing, test your budget against a higher payment scenario

2) Get a smart pre-approval (and ask better questions)

A pre-approval is more useful when it answers the questions that cause last-minute stress.

Ask your lender or broker:

- What documentation will strengthen my file?

- What rate-hold options exist and how long do they last?

- What could reduce my approval amount (debts, income type, down payment source)?

3) Track the right market indicators

Use a simple watchlist so you’re not reacting to every headline:

- MLS HPI trend (city/region where possible)

- Inventory context (balance matters more than one month of sales)

- A second index for cross-checking (e.g., Teranet–National Bank)

4) Match your strategy to your region

- In softer markets, you may have more room for conditions and negotiation.

- In resilient markets, prioritize preparedness (financing plan, deposit ready, quick turnaround).

5) Build a decision rule before emotions kick in

Examples:

- “We only offer if payment stays under $X and the home meets Y must-haves.”

- “We won’t waive financing unless our lender has issued a firm commitment.”

Bottom line: A clear rule protects you from expensive impulse decisions.

FAQs

Why do Canada home prices look “flat” nationally but still feel expensive?

Because affordability is driven by monthly payments and qualification, not just the purchase price. Even modest prices can feel expensive if carrying costs are high.

What’s the difference between MLS Home Price Index Canada and average price?

Average price depends on the mix of homes sold. The MLS® HPI is designed to track typical prices by comparing like-with-like over time.

Are we really seeing a regional housing market split in 2026?

Yes. CMHC expects Ontario to be weaker (and the only region expecting price declines in 2026), while the Prairies and Quebec are expected to be stronger than historical averages.

Is Winnipeg real estate growth actually happening in 2026?

One widely cited repeat-sales index shows Winnipeg up +4.6% year-over-year from January 2025 to January 2026.

Does an Ontario slowdown mean I should wait to buy?

Not automatically. Timing depends on job stability, down payment, and how long you plan to stay. In softer markets, you may have more negotiating power—but you still want a payment you can live with.

Which data should I trust most?

For buyers, the most useful data is local and comparable (city/neighbourhood + property type). National stats are helpful context, but they can hide big local differences.

The bridge: why a mortgage pro can save you real money (without guessing)

Housing headlines are broad. Mortgage decisions are personal.

A licensed mortgage professional can help you pressure-test the stuff a generic calculator can’t fully capture, like:

- income type nuances (salary vs. self-employed)

- down payment sourcing and documentation

- debt-to-income pressure points

- timing (closing dates, rate-hold windows)

- realistic conditions to use in your offer

If you’re comparing options across multiple lenders—not just one—you can often spot trade-offs earlier (payment risk, penalty risk, qualification risk) and make a cleaner decision.

Bringing it home

In 2026, the story isn’t just “up” or “down.” It’s uneven.

Understanding the hidden gaps in Canada home prices in 2026 helps you:

- ignore misleading national averages

- focus on the indicators that match your actual market

- build a mortgage plan around payment comfort—not hope

Top 3 takeaways:

- Local beats national. City + neighbourhood + property type is the real signal.

- Index beats average (most of the time). Average price can be thrown off by what is sold.

- Payment clarity beats price predictions. Your budget is the strategy.

If you’re buying, relocating, or renewing in 2026, don’t guess. Book a short call with a licensed mortgage professional to map your payment range, rate-hold options, and offer strategy.